HF&G - SEPTEMBER 2021 - ISSUE 20 - OIL VS GRETA

Uranium has been in a raging bull market which propelled our basket of uranium stocks sharply higher. Next up: a bull cycle in oil?

Since February 2020 HF&G has been writing about energy security on various occasions. In April 2020 (See our post here) HF&G advised investors to get long a basket of uranium stocks. For our subscribers, we told them which four stocks to buy. Below from our April 2020 update:

APRIL STOCK IDEAS

This month we are adding a basket of uranium stocks. For our view on uranium please see our April update.

Just like our gold investments from last month we are going to invest in uranium by picking four micro cap Uranium plays listed in Australia:

Deep Yellow (DYL)

Boss Resources (BOE)

Peninsula Energy (PEN)

Paladin Energy (PDN)

Over the past month, uranium spot prices have exploded higher and our basket of uranium stocks caught fire.

What’s going on? HF&G articulated a thesis in April 2020 that was well known among uranium bulls at the time. The industry had underinvested as prices were too low. Spot prices had not moved much which made it impossible for mothballed mines to come back onstream. The smart folks at Sprott (a Canadian asset management firm) realized that uranium is a small market and a dedicated uranium purchaser could put fuel under the fire. First, it was a 300 million USD facility, and later it was expanded to a 1.3 billion USD facility that was set up to buy uranium. What did spot uranium prices do? They rallied 65% YTD with most of the gains coming late August and in September.

Will this continue? The uranium bulls sure think it will. Uranium is a product with an extended cycle. It might take a decade from development to actual mining and contracting by utility buyers. Utility buyers are the key here and what uranium bulls are focused on: when will they come back to the market? The cost of uranium itself is estimated to be only 3-5% of the total costs of running a nuclear plant. So if the spot price is 30 USD or 80 USD it does not make a large difference to the cost of running the nuclear plant. Contrast this with gas-fired power plants where the input cost (natural gas) makes up 70% of the total running cost. So when natural gas prices spike (as they are doing now) it impacts a whole host of energy buyers.

Now all this might be true but most junior uranium miners will never get to mine. By the time their project has finally cleared for construction (let alone production) uranium might be in another bear cycle. That’s the risk of investing in junior miners. If you want to invest in actual uranium producers you buy Cameco (listed in Canada) or Kazatomprom (listed in London). Or one can now buy the Sprott vehicle in Canada (Sprott Physical Uranium Trust Fund). Sprott will look to get a listing in the US in 2022.

Uranium is the key ingredient for nuclear plants. Nuclear plants create nuclear waste and there have been a few accidents (Tsjernobyl and Fukushima) which have made the sector very unpopular with large portions of the population. Germany, Belgium, Japan have all promised to go nuclear-free and close all nuclear reactors. The problem is the replacement to nuclear (wind, solar) is intermittent and cannot give the baseload power these countries still need. Battery technology remains light years behind in order for it to store electricity economically. This is the keyword: economically. In essence, this is also the larger debate between the Greta-believers and the Oil-aficionados. The Greta-believers think that we can just make an energy transition by 2025 and phase out all oil-related products. The oil aficionados look at the data and see major problems with the rushed way EV’s and other “renewables” are shoved down policy maker’s (and eventually consumer’s) throats. The issue with shoving things down someone’s throat is: eventually you gag. Let this be what we are witnessing now in the UK and other nations that experiencing somewhat of a rude awakening.

But weren’t we all going “green” by 2025 or 2030? Why do we still care about oil? The issue is that forecasts of the world going “green” has been over-optimistic for decades.

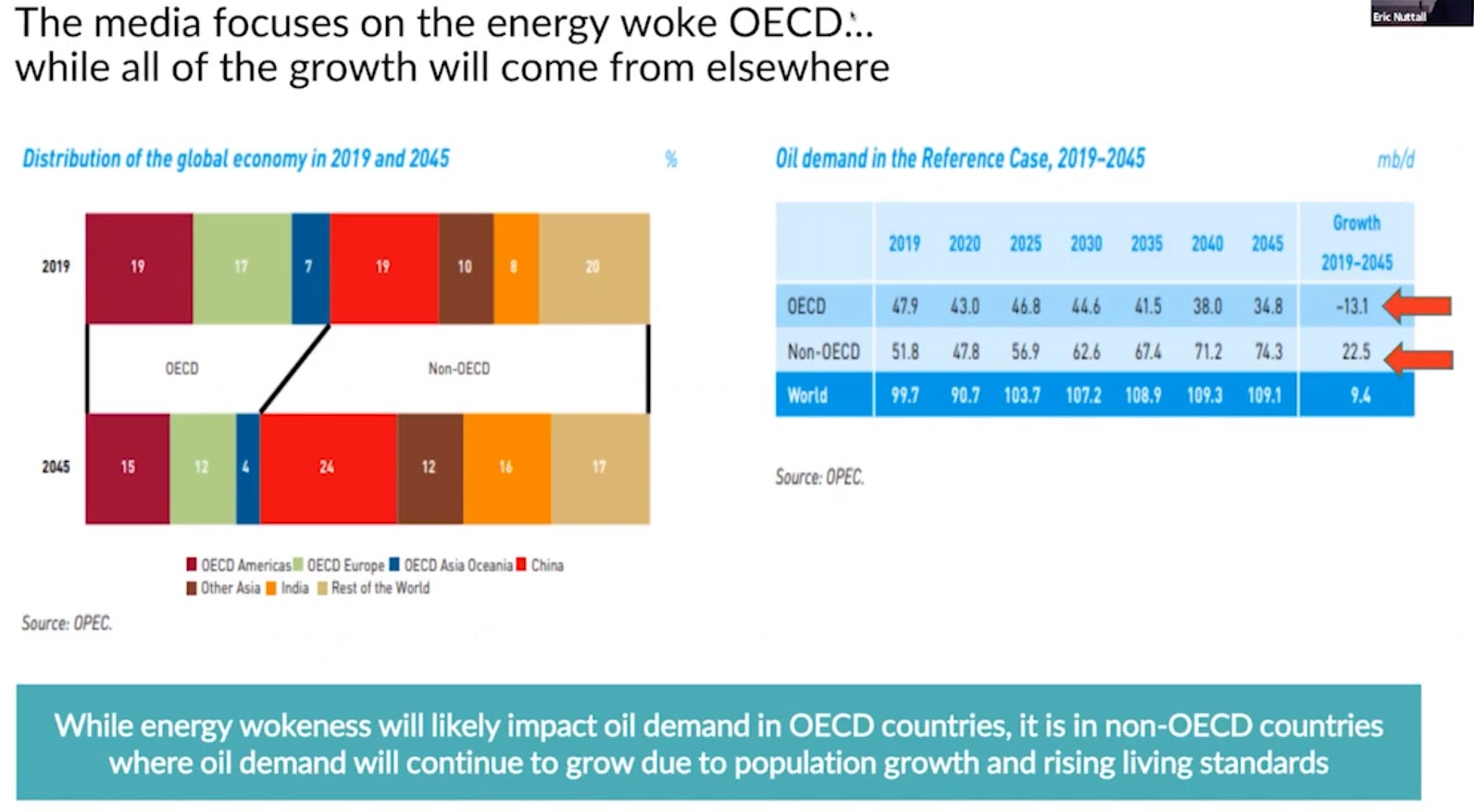

HF&G’s base case is that the transition will happen but will take decades and not years. The growth in energy demand is going to come mostly from non-OECD countries (source: Ninepoint). If you want to follow a great insightful source on oil follow Eric Nuttall @ericnuttall on Twitter.

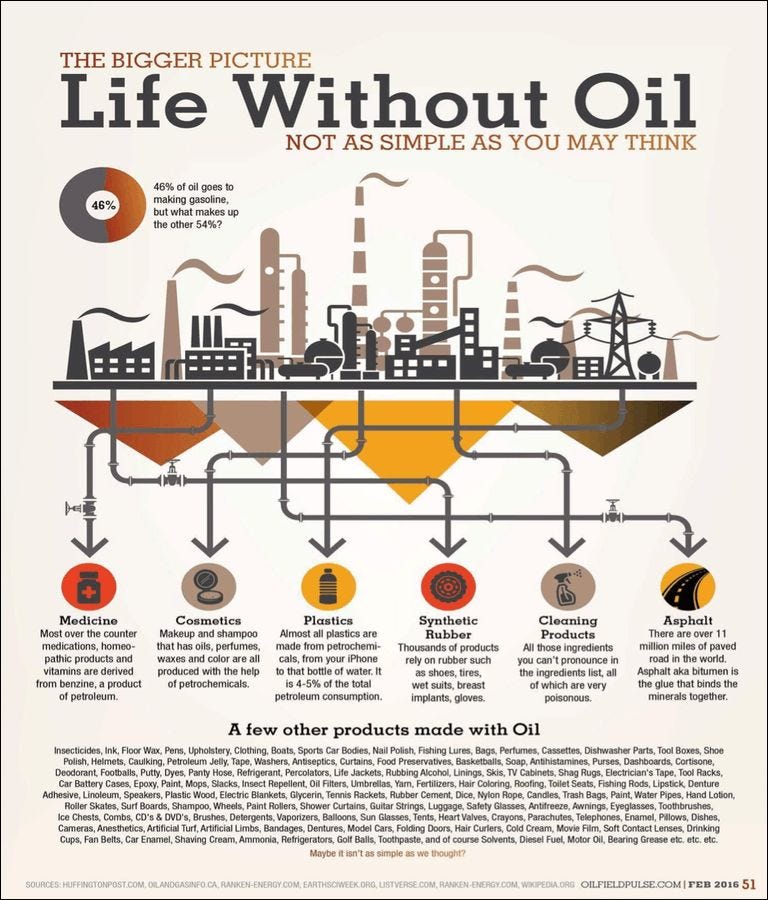

Oil remains essential for much of today’s life although you might not realize it. Please read below overview carefully.

How do we get exposure in oil? While this is not hard in the US or Canada HF&G has always focused on Asian centric ideas. Of our current selection, we have recommended Rex International Holdings (listed in Singapore) twice already and continue to think this is one of the cheapest oil producers globally trading at less than 2x P/E for 2021. We would not be surprised to see Rex have the same performance as Deep Yellow did over the last 18 months by late 2022. When these re-ratings happen they usually occur with violent swings to the upside.

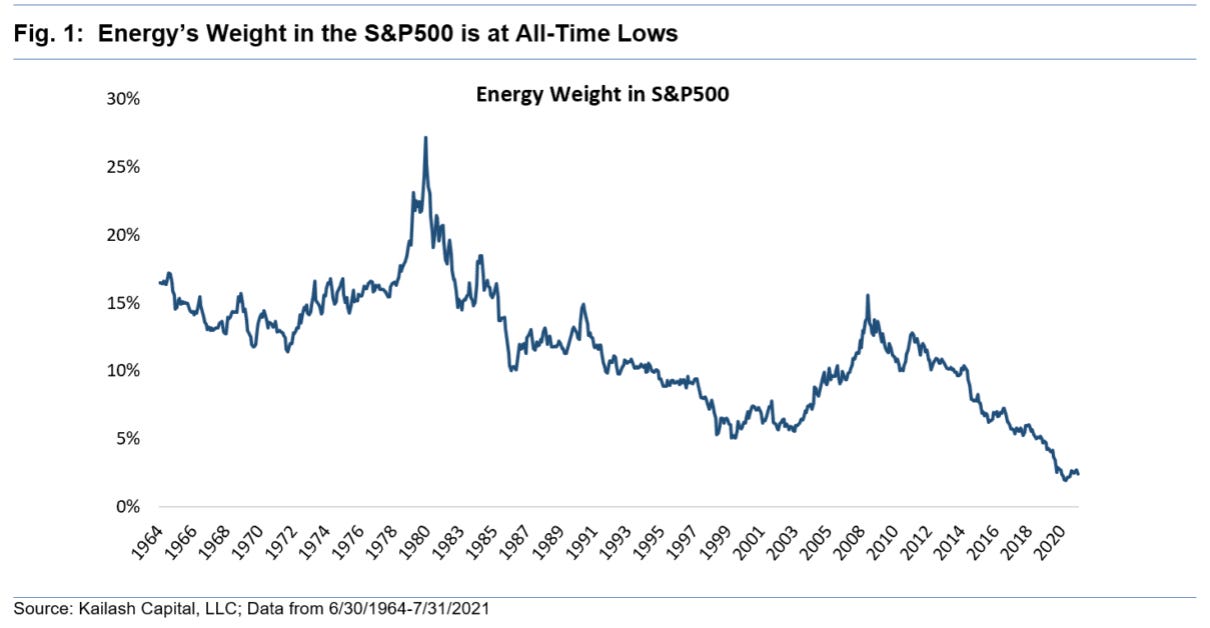

So after uranium HF&G’s call is that oil/natural gas producers will have their day in the sun. The story is similar: underinvestment in oil & gas because of political shaming (greenwashing) and virtue signaling by pension funds and others withdrawing funding from this crucial industry. You can’t run before you can walk and this is what green activists such as Greta are trying to achieve with an impossible energy transition in record time. Finally, the energy weighting in the S&P500 is at an all-time low meaning most investors are not positioned for a bull run in energy stocks. Got Oil?

Don’t believe HF&G? Spend 5 minutes of your day and read Harris Kupperman’s excellent summary of the issue at hand.

PORTFOLIO OVERVIEW

As we do every month hereby our selection.

Of the 29 companies/assets we have recommended since February 2020 three have been sold (documented in previous posts). They have been removed from the list below for editing purposes.

8 companies are down between -1% and -42%

6 companies are up between +50% to +100%

5 companies are up between +4% to +50%

4 companies are up between +200% to +300%

3 companies are up between +400% to +700%

If you are new to the list where would HF&G focus today? 5 ideas.

1) Rex International: this would be the third time recommending this company. It is simply too cheap and a bet on oil.

2) Archtis: see August commentary.

3) Sunpower: energy play in China.

4) Tesoro and Rincon for gold exposure.

5) Tiny Beans for its uplisting potential once it goes on Nasdaq in 2022.

That’s it for this month. Enjoy October(fest)! And as always you can follow us on Twitter @GreedyHuat