HF&G - MAY 2022 - GETTIN' KIRK'D

When one of the largest banks in the world distances itself from a non-controversial speech by one of its employees investors should double down on commodities.

It was a non-event. At least it should have been. A major newspaper hosts a conference in London. Big deal. The Financial Times organizes dozens of speaker events throughout the year. This one was titled: “Moral Money: Turning Talk into Action to hit ESG targets”. There were a series of speakers singing the virtues of ESG and climate action. Enter Stuart Kirk, the global head of responsible investments at HSBC. The title of his speech was: “Why investors need not worry about Climate Change”. Boy, did he have something to say! Please spend 16 minutes of your day watching it in full. HF&G is genuinely surprised the speech is still available on YouTube and has not gotten canceled yet.

The storm that ensued after his speech should have been expected if you are dealing with religious fanatics. Anyone paying attention knows that climate change has become a religion. It is like burning books of the Koran, or the Bible, in religious circles. You need to be punished. Sure enough, Stuart Kirk was ridiculed by the CEO of HSBC and consequently fired. Funny fact: the slides were approved by HSBC senior managers before the FT event. HSBC was a major sponsor of the FT event as well. How many times has someone lost his job for speaking his mind at a conference where his employer is one of the major sponsors? You can’t make this stuff up. Steve got canceled, Steve got Kirk’d!

While traditional religions have mufti’s, rabbi’s and priests the climate religion gang has prophets such as Al Gore, Greta Thunberg, and the IPCC. Don’t believe it’s a religion?COP26 even had Climate Confession Booths.

HF&G has discussed for years how the green energy transition will happen but it will take way longer than investors, regulators, and governments expect. Recently, driving around Southern Italy HF&G paid attention to finding charging points for EV’s. Fortunately, we were driving a hybrid that could also be filled up with diesel as the infrastructure for EVs is just non-existent. The situation is somewhat better in more developed parts of Europe but our random checks at gas stations show us that 40% of chargers are out of service at most times. Let’s now build massive amounts of EV chargers and maintain them in India, Indonesia, Thailand, Philippines, Vietnam, etc. This will be fun to watch for anyone who has been to these countries and knows how dysfunctional energy grids can be.

Nevertheless, HF&G does recognize that EV sales are booming from a low base. According to German research (Joanneaum) in 2019 it takes over 179,000 km before an EV vehicle becomes more environmentally friendly than a modern diesel car. Just Google this topic and you will find many superficial studies that claim the exact opposite: “EVs are cheaper to run than diesel/gasoline cars”. These studies conveniently ignore to paint the entire picture.

While making the batteries, charging infrastructure, and other components for EV the full cost of extracting, operating, and maintaining the required commodities needs to be taken into account.

Once this becomes clear and commodities continue to go parabolic in the current supercycle the cost of EV components is going to increase even more. Don’t listen to HF&G but do listen to the CEO of BMW who warned about it in April this year:

NEWYORK -BMW Chief Executive Officer Oliver Zipse said companies must be careful not to become too dependent on a select few countries by focusing only on electric vehicles, adding that there was still a market for combustion engine cars.

“When you look at the technology coming out, the EV push, we must be careful because at the same time, you increase dependency on very few countries,” Zipse said at a roundtable in New York, highlighting that the supply of raw materials for batteries was controlled mostly by China.

“If someone cannot buy an EV for some reason but needs a car, would you rather propose he continues to drive his old car forever? If you are not selling combustion engines anymore, someone else will,” said Zipse.

He has long advocated against all-out bans on combustion engine car sales in the face of rising pressure from regulators on the auto industry to curb its carbon emissions and environmental impact.

Offering more fuel-efficient combustion engine cars was key both from a profit perspective and an environmental perspective, Zipse argued, pointing to gaps in charging infrastructure and the high price of electric vehicles.

The plans by certain countries to phase out gasoline cars completely by 2025 or 2030 seem highly irresponsible. Perhaps a few very wealthy countries such as Norway or Singapore will succeed in this target. In the case of Norway it is rather hilarious that it is only able to give every woman, man, and dog a massively subsidizes EV because it has vast oil and gas reserves.

COMMODITY SUPERCYCLE INTACT

HF&G believes the commodity supercycle is going to last a number of years as primarily European climate religion fanatics have infiltrated European governments with their idiotic ideas and policies. It will take a few elections to get folks like Frans Timmermans and others to be removed from power by angry voters. Even with the war in Ukraine demonstrating the EU’s completely failed energy policy, there are still (mostly) green parties advocating for the closure of nuclear energy plants in Germany, Belgium, and Sweden. You simply can’t make this stuff up. In Germany, it is even more painful to watch that there are actually abundant gas resources within its domestic market. In order to unlock this gas fracking techniques need to be used but cannot be discussed at all for dogmatic reasons. Last month HF&G noticed for the first time that the state of Bavaria was sounding the alarm bell:

Germany should look into the option of using fracking technology to extract domestic natural gas in light of the energy crisis exacerbated by Russia’s war against Ukraine, said Markus Söder, premier of the southern German state of Bavaria in an interview with the Funke Mediengruppe. “We have to examine what is possible and reasonable with an open mind,” said Söder. “As representatives of the people, we even have the constitutional duty to keep an unbiased eye on all options in such extraordinary times of crisis.” Söder said the United States had made itself “completely independent of the Middle East” through fracking. Opposition among the population and strict regulations have made substantial use of fracking in Germany highly unlikely until now. “Bans could be lifted,” Söder said.

If you don’t have commodities in your portfolio please do not fall for the absurd sentences: “It is too late now, they have already run”. No, they have not. Oil prices are back at 120 USD yet oil stocks remain in deep value territory as many large investors cannot own oil stocks due to ESG and other “greenwashing” rules. Just like tobacco stocks outperformed overall markets between 2000 and 2010 HF&G thinks the same is about to occur for commodity stocks in the coming years. There could be sharp pullbacks along the way but the overall trend is upwards and to the right. Buy a basket of coal, uranium, oil, gas, copper, zinc, aluminum, and gold names.

PORTFOLIO REVIEW

In March we reviewed the entire portfolio so please visit the March review as not much has changed apart from one Crypto Tulip (Chainlink) getting cut in half vs our purchase price. Other cryptos have held up well vs our purchase price. Overall markets in the US might have imploded by you wouldn’t notice it from looking at uranium stocks, Oriental Watch, Rex, etc.

HF&G is adding a new very “dirty stock” to its portfolio in May. Read below for more details.

While HF&G has discussed the energy investment deficit at length this month we will add the dirtiest of them all: Mongolian Coal!

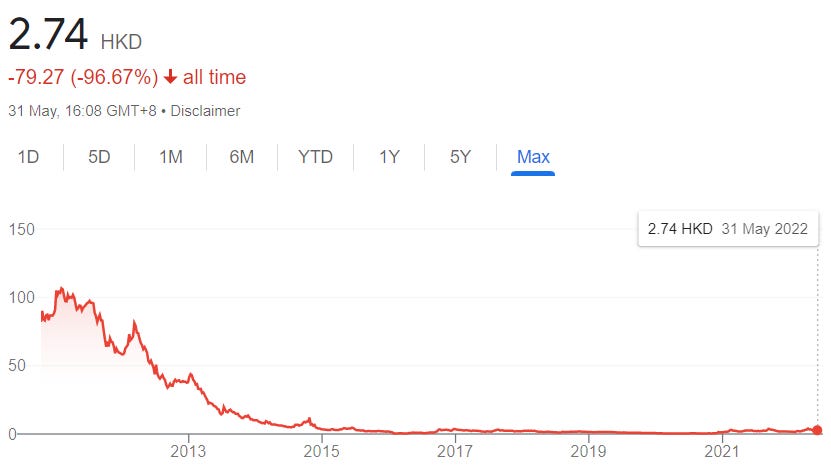

This idea came to us from Wickhams Hill (who also tipped us on ISSP in April last year). While ISSP has lost some steam we think Mongolian Mining (975 HK) has the chance to go parabolic in 2H22. HF&G has been aware of the Mongolian Mining story. First and foremost new investors should know this stock is down 97% since its peak a decade ago. MM was listed in 2010 and had a $4 billion market valuation at its peak. The stock was covered by every major brokerage house. Fast forward to 2022 and the stock has a market value of just over $300 million. Not a single broker covers the company.

What’s changed to make it attractive going into 2H22?

After years of fighting between Mongolian and Chinese officials, it was finally agreed in October 2021 on what sort of rail connector would be used between the two countries. The rail line is not completely finished yet but this should occur in 3Q22 and meanwhile, we can see daily increases in trucking volume across the China/Mongolian border.

China has an interest in Mongolian coal so it can reduce its dependency on seaborne coal from both Australia, Indonesia, and the USA. This is the crux of the story. Sattelite images viewed by HF&G make it clear the railway connection construction is in full swing and should be finished by July and commissioned by September. So while we are unclear if there could be further delays we think the trajectory of EBITDA growth could be significant.

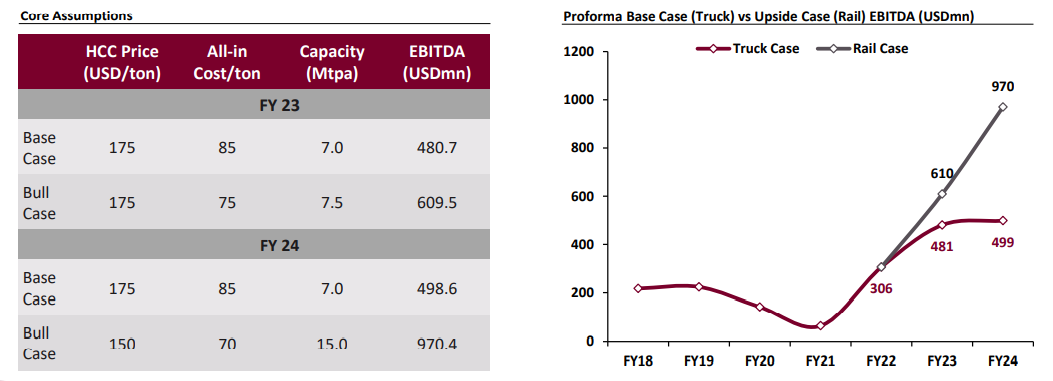

Our latest channel checks suggest cross-border trucking volumes will total over 750K tons in 2Q22 vs just 361K tons in 1Q22. In 2H22 this should improve to close to 2M tons! If these numbers are correct the FY22 EBITDA could be anywhere between 400-550M USD depending if coal prices maintain above 300 USD or not. Even at significantly reduced coal prices EBITDA growth would be significant. All this indicates that on an Enterprise Value basis MM could be trading around 2x EV/EBITDA.

Longer-term the company thinks it could produce over 7M ton of coal per year. Even assuming spot prices get cut in half the EBITDA would be astronomical vs its current market cap. Needless to say, it would have no issue servicing its debt and interest payments which continue to worry market participants.

MM’s stock is now just under 3 HKD but if the above scenario materializes could easily surpass 10 HKD in 2H22.

This is a high-risk investment idea with many moving parts and China’s absurd zero-covid strategy could derail demand for coal. Sudden changes in sentiment towards Mongolia by China, a newfound love for Australian coal, or better relationships with Russia could lead to sharply lower coal pricing going forward.

That’s it for this month. As always, you can find us on Twitter @GreedyHuat for ad-hoc commentary on stocks, energy, and commodity markets.