HF&G - MARCH 2021 - ISSUE 14 - DON'T BE BILLY HWANG...

...as Billy ran his family office like a casino and the drunken dealers were Nomura, Credit Suisse & co. For this month's stock idea, we descend into the world of classical music.

The first quarter of 2021 ended with a bang in financial markets. Convicted for insider dealing in 2012 “trading genius” Billy Hwang blew-up his “family office” Archegos. Kudos to Nomura, Credit Suisse, Goldman Sachs, and surely a host of other investment banks who would have sold their proverbial mother to make an extra dime from Billy.

The entire concept of a family office should be that you take prudent care of your family’s assets. Judging by the Financial Times and WSJ reporting HF&G doubts Billy was very prudent with his family’s capital. According to press reports his assets grew from $200 million in 2012 to $10 billion this year. He then leveraged this 5x so he was investing with +/-$50 billion in mostly CFD’s (Contract for Difference). These instruments do not have to be disclosed to regulators and are like dynamite if they go against you. His strategy was to invest in various Chinese tech companies including suspected frauds like GSX Techedu. GSX has been exposed as a fraud by MuddyWaters and a host of well-respected short sellers. The stock is now -38% YTD. Even after the drop this “company” still has a market cap of $8 billion.

In short: if you like to sleep at night and truly look after your family capital you don’t have to be Billy Hwang. You don’t have to invest in CFD’s and there is no need to put on 5x leverage.

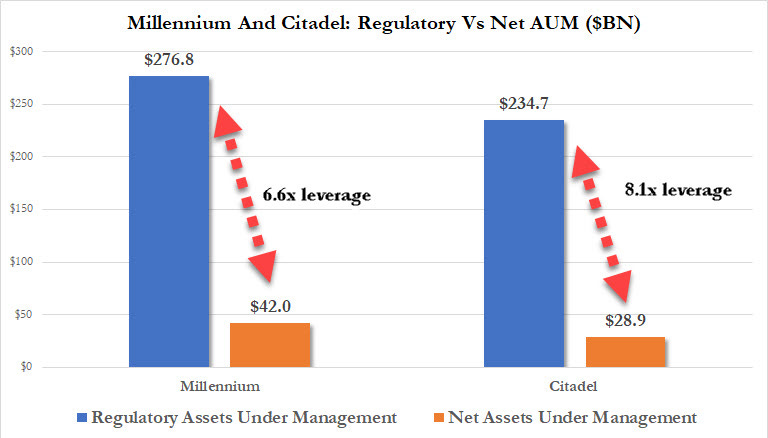

Speaking about leverage, according to an article by ZeroHedge (an excellent website!) very large investment players like Millenium and Citadel are running their shops on even higher leverage. What could possibly go wrong?

CREDIT SUISSE: AMONG THE WORST?

Why is it that the same banks get intertwined again, and again and again when the sh*it hits the fan?

Let’s look at Credit Suisse’s stock chart (source: Refinitiv) over the last 20 years.

The share price finished around 10 CHF recently declining from 87 CHF in 2007. During the biggest financial crisis in recent memory (2008), the stock bottomed at 21 CHF. Over the ensuing 13 years, the stock was again cut in half! Credit Suisse has essentially been a 20-year train wreck for its shareholders yet in 2021 alone it will likely lose $3 billion on Greensill and another $3-7 billion on Billy Hwang. These two events alone have essentially wiped out all the after-tax profits from 2018-2020. This is on top of the $10.4 billion in fines it has paid between 2000-2020!

At what point does the realization set-in that Credit Suisse is being run as some sort of illegitimate scheme rather than a prudently managed bank? The fines described above are on top of the regular taxes the banks pay globally. No wonder the share price has been decimated as after all taxes and fines not much is left for shareholders to chew on. If all board members and management were partners in the bank and had significant skin in the game financially via their shareholdings would we see the same outcome? Posing the question is answering it. Bottom line: if you look for a bank to have your financial dealings with chose a boring one that does not deal with characters like Billy Hwang. In Switzerland, this could potentially be Raiffeisen. As bank shareholders and customers, the Billy Hwang example once again shows banks are black boxes where even the managers do not understand the risks they take. HF&G has no banks in its selection and for good reason.

SMALL IS BEAUTIFUL

HF&G has been sharing a selection of small and medium-sized companies for over a year. Speculators like Billy Hwang will continue to blow up in the future but fundamentally this has no impact on the business affairs of the companies discussed by HF&G. If you are making leveraged bets this can only happen in large liquid names, not in small and medium-sized companies. Although, Cathy Wood from ARK might have a different opinion on this topic and is potentially creating an explosive situation at her ARK ETFs as demonstrated by the Bear Cave (an excellent short-seller letter).

This month our portfolio review will be published only to subscribers. For less than 1 dollar/day you get a monthly update and stock ideas sent to your inbox on the last day of the month. Please also follows us on Twitter @GreedyHuat for sporadic stock commentary.

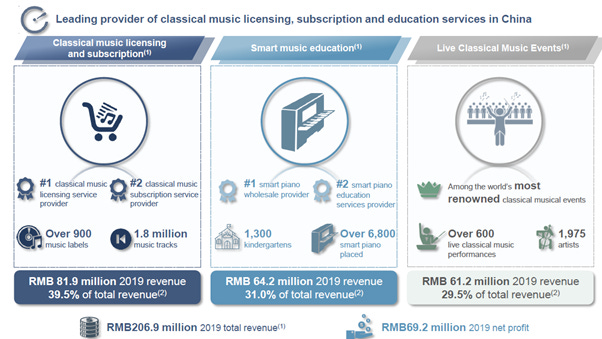

Last month we shared our monthly pick only with our subscribers but this month we will publish it for all to read. HF&G will be adding a small Nasdaq-listed company with its operations in China to our list: Kuke Music Holdings (ticker: KUKE). Recently, the company had a market cap of about $195 million as it has been trading 30% below its 10 USD IPO price.

Kuke’s business consists of three pillars:

Kuke was listed early in 2021 and will report its FY2020 results in about 10 days’ time. The company was brought to our attention via our network of Chinese investors who have followed the company for multiple years while it was private. The main driver for Kuke is the Chinese government policy’s decision to stimulate the mandatory education of classical music from kindergarten to primary school and high school. We quote from a BOCI research report published on 19/10/2020.

PE, arts and music to be included in the high school

entrance exam, according to the MoE

The Ministry of Education (MoE) announced to further enhance the importance of

physical education (PE), arts and music for the all-round development for the

younger generation. To raise the awareness of the importance of PE, arts and

music subjects, the MoE intended to include PE, arts and music as scored subjects

in the high school entrance exam as well as in the academic proficiency test in high

schools. In particular, for PE subject, the MoE will gradually raise the total score in

the future and eventually the weighting for PE subject in the high school entrance

exam may become the same as key subjects like Chinese, maths and English.

Currently, many cities have already included PE as one of the scored subjects in

their high school entrance exams, but only a few cities have included arts and

music as scored subjects in the high school entrance exam. It is expected for arts

and music to be included as scored subjects for high school entrance exam in most

of the cities starting from 2022 at the earliest.

Decades of investing in China have shown that when the Chinese government implements a nationwide directive in education it is worth it to pay attention and look for investment opportunities.

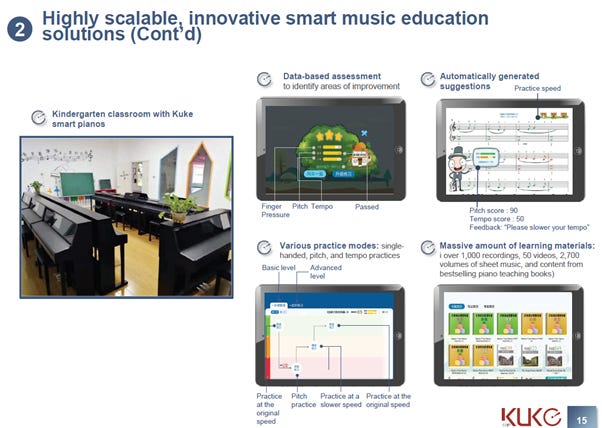

The key investment merit of Kuke is its proprietary Smart Piano system. The piano is the most popular instrument in China. Via Kuke’s system pianos are purchased by schools in group purchases. The schools do not pay for the pianos (Kuke bears the cost of production and installation) but Kuke makes money on a pay-per-usage basis. The roll-out of the piano system is accelerating but hit a speedbump in 1H20 due to Covid restrictions in China. As per the prospectus the company had 30K students and 6K pianos deployed but this should grow to over 11,600 pianos by late FY2021.

Private tutoring of piano lessons can be expensive and inefficient as there is a shortage of piano teachers. Kuke’s Smart Piano system offers a solution to this problem.

Interestingly, Kuke has a long-standing relationship with Naxos. Naxos is a company founded by Klaus Heymann, a German national who has lived in HK for over 40 years. Heymann has built up the largest classical music catalogue in the world. The value of the Naxos brand alone is probably worth multiple time’s Kuke’s current market cap. We imagine that publicly listed music players like Sony, Tencent Music, UMG, or Warner Music are all tracking Kuke closely. Once further ownership discussions between Naxos and Kuke are cleared up going forward HF&G would not be surprised if Kuke changes its name to Naxos eventually.

Early March Kuke participated in an education conference organized by Morgan Stanley. After its FY20 results are released in April we would expect more attention to come to the company as its business model is poorly understood. There are currently no consensus estimates on the company so HF&G has made their own based on the continued roll-out of the Smart Piano system. On our estimates, Kuke trades at 10x 2021 EPS and just 7.5x 2022 EPS. If our assumptions are ball-park correct we see a scenario where Kuke trades at 15-20 USD rather quickly.

Risks to the Kuke story are a slower than anticipated uptake in the Smart Piano adoption or increased competition. Currently, we are aware of no other publicly listed company that offers a similar service to its customers.

That’s it for this month, enjoy April!