HF&G - JUNE 2021 - ISSUE 17 - DELTA+ FEAR

Endemic vs Zero-Covid is the ongoing policy battle as Delta+ has become the "variant of the day". Our June pick is an SGX listed re-opening play.

As we approach mid-year 2021 we have a clear trend which HF&G already touched upon numerous times. Those countries that are finally realizing Covid is endemic and those in denial. This new reality is again going to create winners and losers in the market.

On the one hand we have the US/EU which are moving on with life despite hundreds of “cases” popping up across various US states or European countries. Lately media reports are going wild about “The Variant Of the Day” called Delta+. Judging by newspaper headlines across Europe Covid-19 is not the main story anymore despite radical efforts by some long discredited virologists to keep the fear mongering alive. The public is finally catching on that all the doomsday models predicted by “the scientists” have been largely wrong and exaggerated (see DailyMail frontpage 29 June 2021).

In the rest of Europe soccer stadiums are (semi)full for the Euro2020 with Budapest taking top spot in terms of crowd (67,000 maxed out crowd) with no restrictions or masks.

On the other side of the globe we have Australia continuing its rolling lockdown experiment which, according to HF&G, is going to fail miserably. You can’t have a zero-covid policy, just like you can’t have zero flu policy. According to the WSJ China also alerted the world that it will remain locked-off from visitors for at least another year.

Surprisingly, Singapore has gotten the message and late June the three up-and-coming minsters penned an opinion piece in the Straits Times.

For Singapore to go from basically Zero-Covid policy to “We have to live with it” is a huge step. What prompted this? An exodus of foreign key business leaders? Singapore is a fantastically efficient business hub but the word “hub” means travelling to/from the hub with great ease. HF&G remains hopeful that after August 9th National Day the ministerial task force will have a plan to truly open up. First, we need to get there with another month of silly rules from the ministry of silly walks (dine-in limited to 2pax, no music allowed during dinner, wearing masks outdoors, etc). HF&G has often commented on all these rules and how they are made up with zero scientific basis and which is why populations will lose their patience with politicians and the scientists that guide them. HF&G is not advocating violence of any sort but in the UK it is happening with Chief Medical Officer Chris Whitty being attacked on the street.

So how do we position our portfolio’s for the eventual Asian/Singapore re-opening? Some re-opening plays have rallied hard while others have not. On the SGX we find our June idea (hat tip to Wickham’s Hill for bringing it to HF&G’s attention).

mm2

The last year has created an almost unprecedented environment of winners and losers - distortions of the playing field never seen before. There have been the stay-at-home stocks, the reopening stocks, meme stocks and the inflation trades. Developed markets have been eager to ‘look-through’ short-term disruptions and price-in a full recovery. While in some emerging markets the struggling companies have been left behind. Mm2 Asia Ltd. is one of those companies.

As a successful film production, live concerts and events, and leading cinema business in Singapore and across Asia, mm2 has grown revenue from S$38.4 to S$268.7m in the 5-years leading up to COVID.

The core business of film and content production grew from S$29.8m to S$78.7m over the same period due to the burgeoning demand for local content particularly in the Taiwanese and HK market.

The cinema business built a strong position as a leader in Singapore and the third largest player in Malaysia. Through acquisitions, these grew from S$4.8m to S$101.1m in turnover during the same 5-year period.

During its rapid growth, mm2 had accumulated debts of almost S$342.7m as of March 20 compared to next to nothing, just a few years earlier. The borrowing facilitated growth in the production business to meet demand from content companies and Southeast Asian distribution through the cinema business. The business was just gathering the momentum to begin repaying their debts when COVID hit and led to rolling travel restrictions and a domestic lockdown.

As production sets were shut down across Asia and cinemas closed during Singapore and Malaysia’s lockdowns, revenue fell more than 90% during 1H21 (March – Sept 20). The remainder of 2020 was not much better for mm2 with only limited cinema openings and major operational limitations in the production business.

Between the beginning of 2020 and early 2021, the share price fell 75% and the company was in a semi-distressed state, having announced a deeply discounted and fully-underwritten rights-issue to repay debt obligations.

At its nadir, the share price reached S$0.055 immediately following the rights-issue in April, down 85% from the 2017 high. However, somewhat inline with the expression that its always darkest before dawn, the right-issue was a watershed moment for the company and significantly ‘derisked’ the pathway to recovery.

While near-term revenue was volatile, we took the view that liquidity risks were now behind the company and despite little visibility on earnings, there was a clear plan to realise value through a spin-off of the cinema business which meant investors participating in the April rights-issue at $0.065 were effectively getting the fast growing and profitable production business for free.

The company’s full year results were released earlier this month and revealed a much stronger financial position following the rights-issue and retirement of the medium-term note, partly helped by better than expected operating results in the Cinema and Film production business.

The reopening of economies is inevitable and living with COVID just a part of life going forward. Asia has been behind in reopening, with the most vulnerable populations and inadequate healthcare systems. The above mentioned opinion piece by Lawrence Wong (key contender to be Singapore’s next prime minister) makes mm2 an attractive SGX listed recovery play.

This shift is a major development for mm2, which was still operating with the lingering risk of snap lockdowns that would impact the domestic cinema business in particular which is now just breaking even. Furthermore, this would open-up Singapore as a hub for regional concerts and events, as the company has highlighted on the most recent call.

mm2 still trades at a distressed valuation, however confirmation of the company’s recently improved performance is likely to be what this stock which has been left behind needs to catch-up. mm2 closed at 0.068 SGD and could be a double or triple on a 12-24 month horizon.

Portfolio Review

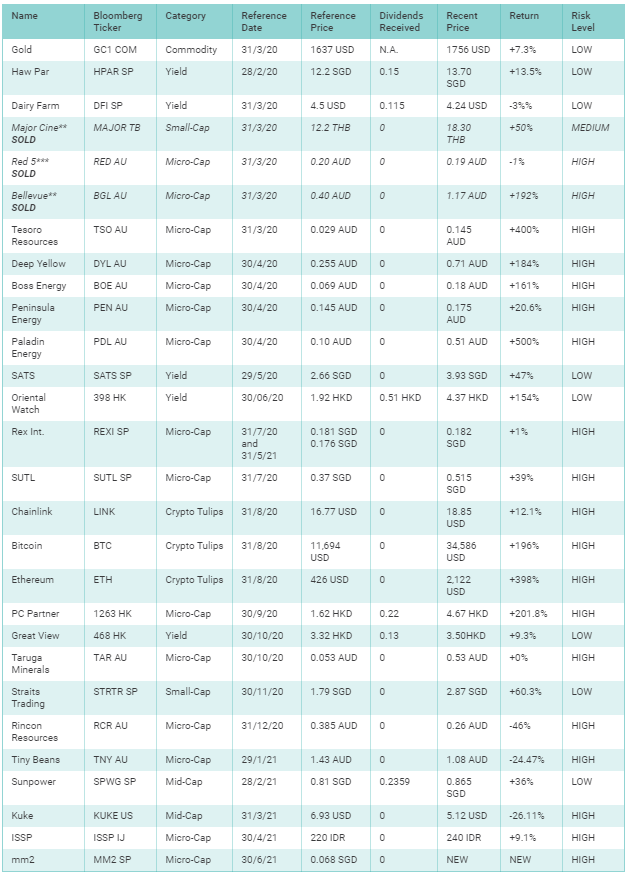

Finally, below we give an overview of our picks since February 2020. This month we are axing another gold stock which has massively disappointed. Red 5 is led by an incompetent management team from everything we have seen over the past 18 months. Luckily the stock closed June almost at our purchase price so our loss is minimal. The only hope for Red 5, in HF&G’s opinion, is that the company gets acquired and the overpromising management team gets replaced.

To re-cap so far we have sold:

Major Cineplex (+50% gain)

Bellevue Gold (+192% gain) and now

Red 5 (-1% loss)

In the rest of our selection we note the sharp pullback in Tesoro Resources. TSO is preparing to release its Maiden Resource Estimate (MRE) in the coming 30 days. The initial excitement about its El Zorro project saw the stock reach over 0.50 AUD in 4Q20. Early 2021 the company completed a capital raise at 0.27 AUD but since then the stock declined almost 50%. Investors have gone from greed to fear. HF&G now believes risk/reward in TSO is very attractive again as the initial MRE might only be around 700k oz (HF&G estimate) but this is just a starting point and the asset will grow over time.

In Crypto land massive spikes are followed by large downdrafts. The level of speculation and volatility is only for those with a strong stomach. Case in point: Chainlink was 4.74 USD one year ago, peaked recently at 52 USD in early May 2021 and at the time of writing was around 18 USD. Since we added some Crypto exposure to our list Bitcoin and Ethereum have outperformed Chainlink but given the volatility this could change at any point.

In the Uranium space our basket of uranium related stocks has rocketed higher. Paladin Energy is up over 500% since we added it to our list. Remarkably, the uranium spot price has barely moved and is still around 30 USD/lb. Longer-term uranium remains an attractive asset given the clear benefits nuclear power has over alternative energy sources.

Finally, both PC Partner and Oriental Watch have announced massive profit alerts and paid (or announced) great dividends. We expect great results and dividends to continue for both.

As always you can follow us on Twitter @GreedyHuat for occasional commentary on stocks, general ideas or debunking of Covid hysteria. Enjoy the Summer and see you all late July.