HF&G - JULY 2021 - ISSUE 18 - WHO IS HEALTHY?

July was a wild month for China tech names and an a fascinating month as we learn more about the concept of a "health pass". No new picks but a quick portfolio review.

July was a wild ride if you are invested in Chinese tech names. HF&G has shied away from any Chinese tech companies as it is hard to understand Beijing’s long-term plan for its billionaires. Recall, Jack Ma and the infamous failure of Ant’s IPO. Jack Ma has not been seen in public regularly ever since. HF&G received below “meme” describing the situation being a foreigner investing in Chinese stocks. All of this reminds us of being an investor in oil & gas names in Russia: if you are not highly informed who is in/out of favor with Mr Putin you might wake up one morning where your stock has stopped trading and the company nationalized.

WHO IS HEALTHY?

Over the past month several countries have started to introduce mandatory “health passes” for large events, restaurants, museums, concerts, etc. HF&G is interested in the topic as it has serious investment implications for many industries we could potentially invest in. Let’s have a closer look at the issue.

Denmark was first in May, followed by Austria and recently France and Italy joined the club. HF&G suspects the rest of Europe will not be far behind. The name “health pass” is curious as it only checks one thing: if you have been vaccinated against Covid, or recently tested negative. In essence, you can be 165cm tall, weigh 237kg, test negative for Covid and you are allowed to enter the restaurant order your steak, fries, ketchup and 12 beers. Once outside the restaurant you could have an intoxicated drive home.

If we apply the “Covid” playbook logic the right formula would be that before you enter a restaurant you were asked to stand on weighing scale. They would also measure your height and your BMI (Body Mass Index) would be calculated.

If your BMI was “positive” (yellow, orange and red zone) you would be isolated in a mandatory health facility for two weeks and put on a stringent diet and exercise routine. Only if you tested “negative” after two weeks (green and blue zone) would you be released again. If you continued to test “positive” you would be required to stay longer until you were no longer a danger to society. Remember, if many obese people all had a heart attack at the same time it could overwhelm our ICU capacity. Recall, that according to the CDC obese people are at much higher risk of Covid than others as well.

Adults with excess weight are at even greater risk during the COVID-19 pandemic: Having obesity increases the risk of severe illness from COVID-19. People who are overweight may also be at increased risk. Having obesity may triple the risk of hospitalization due to a COVID-19 infection.

In light of this: how is it in anyone’s interest that the world over gym’s and other sport venues have been closed for months? On the flip side “essential services” like fast food restaurants were always allowed to stay open.

Get the picture? We could go on here.

HF&G has continued to argue for over a year now that the unique focus on one pathogen (Covid) and total disregard for all other health related considerations is literally insane. Being healthy is more than Covid. When the WHO was founded in 1948 the definition of “HEALTHY” was:

“A state of complete physical, mental and social well-being and not merely the absence of disease or infirmity”

Meanwhile it is becoming more evident by the day that the extreme measures instituted against Covid are having all sorts of nasty side-effects on society:

So Singapore had 452 suicides in 2020 vs 29 Covid deaths. Enough said.

How about the impact on children? Children are becoming obese at record rates as they are forbidden to exercise and school extra-curricular activities are curtailed.

And recently, a tragic violent act by a high school student in 4th grade against a school student in first grade with terrible consequences. Even the education minister admitting that the continued stress on children had gotten too extreme. We can’t be certain this is only due to Covid but the mental stress put on children with all the absurd social distancing and mask-wearing mandates in school is probably not helping for their well being.

Remember how it all started to “flatten the curve” so ICU’s would not be overwhelmed but it seems to have morphed into something completely different. We are now asking kids to get vaccinated against a disease they are at little to no risk of getting seriously ill from yet find it normal that we restrict their movements and usual child behavior and allow them to eat unhealthy food and consume sugary drinks without any control? HF&G thinks the long-term effects of this continued fear-mongering about Covid variants will have a long-lasting impact on consumer behavior and preferences. The introduction of health passes is going to create havoc in many industries which are sometimes already priced as if everything returns to normal asap. Buyer of travel, leisure, airline and related sectors beware.

PORTFOLIO REVIEW

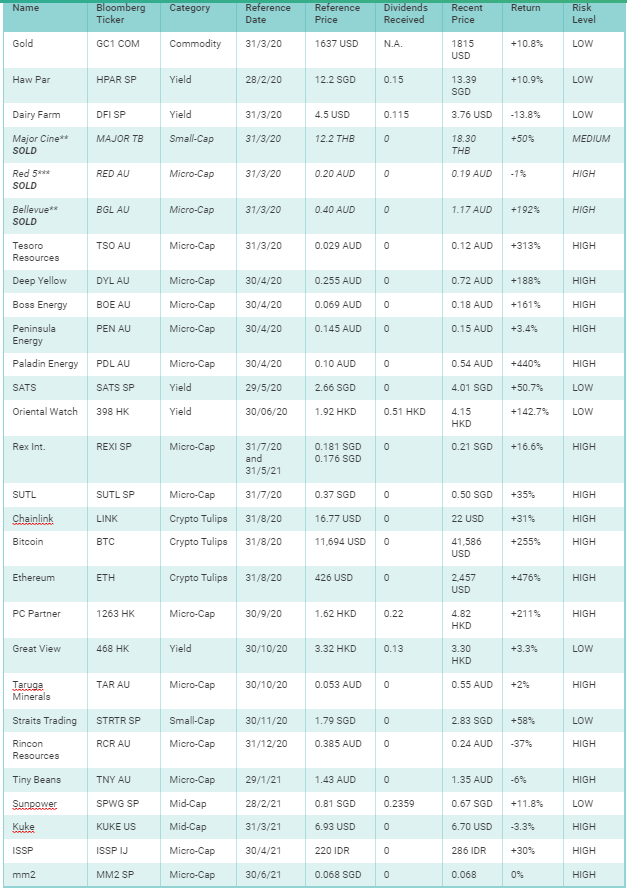

As every month we share the performance with all readers since February 2020. HF&G has had a number of multibaggers and very few losers so far. Profit has been taken in three ideas while all the rest we continue to track.

Let’s look at the entire list and give an update:

Gold continues to be a core long given the incredible amount of money printing by central banks globally. If you don’t own some gold yet, it is not too late. Another way to play the gold theme is via gold equities but here the risk is much higher. When you invest in junior mines please recall that 95% of all mining projects fail. There is only 5% that ever makes it into production and picking a winner is very hard. Most junior resource companies run out of money, do not get permits to develop the mine, have a project that is uneconomical at current commodity rates, get nationalized by the local government, has fraudulent management or a combination of all the above.

All that being said we have sold our stake in Bellevue Gold at a significant profit and made a tiny loss on our sale of Red5. The two remaining gold explorers are Tesoro (Chili) and Rincon Resources (Australia). Tesoro just published its MRE (Maiden Resource Estimate) over the past week and the market was disappointed by the result. Tesoro’s MRE was 660,000 oz as a starting point. HF&G thinks Tesoro is now great value again as the El Zorro project is large and will surely grow going forward. Insiders are buying over the past week and with the stock now down over 50% from the last capital raise in December at 0.27 AUD there is good value here. Rincon is a different story as 8 months after its IPO the company has yet to produce a drill hole from its Hasties project in Western Australia. If the drill holes are successful expect the stock to rocket higher, if no commercial deposit is uncovered Rincon might not have enough cash to continue in its current form. Investing in junior gold miners is risky and should be sized accordingly.

Some of our strongest performers are our basket of Uranium stocks. Paladin, Boss and Deep Yellow are all up triple digits which is a great outcome. Peninsula Energy is a laggard. The rise in the uranium miners is due to a change in sentiment as the uranium price has barely budged from 29 to 32 USD/lb. The long-term story of uranium continues to be one of underinvestment in uranium supply which will lead to higher prices down the line. We will hold onto our uranium basket but would not add to them at current prices until we see a sustained move higher in the uranium price.

SATS is our way to play the re-opening of Singapore. SATS has a monopoly position at Changi airport. Singapore has said it will open up some travel from September onwards but we are very cautious as the Singapore government has had to walk back promises of re-opening its skies multiple times already. If travel does not pick up SATS is expensive on its current earnings profile. If one believes that travel can not restart before large parts of Asia are vaccinated below infographic from the Straits Times should give you some pause.

Oriental Watch has morphed from a HK luxury watch story to a domestic China luxury watch story. While three years ago 70% of its sales were in HK, in 2021 this is now 70% in China. China will keep its borders closed for another year according to WSJ reports which means Chinese citizens will have to spend domestically rather than internationally. Oriental Watch is the largest importer of Rolex in China and saw its sales double in FY21. The stock has reacted accordingly. Oriental Watch is also a great dividend payer with an expected dividend yield between 8-10%. HF&G believes Oriental Watch is now worth at least 6 HKD/share.

Rex is our SGX listed oil-play. We just wrote about Rex a few months ago and not much has changed. We will get 1H21 results published in August and expect the market to be surprised by the cash flow generated from its Oman assets. Rex remains a clear buy at these levels. HF&G expects the stock to double from here.

SUTL is dirt-cheap operator of luxury marina’s in Asia but lacks news flow as all its projects have been postponed by Covid. SUTL continues to trade at negative enterprise value which makes no sense.

In Crypto land we have seen the yo-yo movement continue. There’s nothing to change our thesis on Bitcoin, Ethereum or Chainlink. We would continue to hold this basket of crypto’s to gain some exposure. Please only invest in Crypto if you can stomach the volatility. While not on our official list (and we will not track it in the future) there is a Canadian company (Voyager Digital) which is crypto trading platform that looks interesting way to play the crypto theme.

Adjacent to the crypto theme is our investment in Pc Partner which supplies GPU’s to the crypto and gaming market. The stock has rallied over 200% since we wrote about it and we continue to think the stock will do well going forward. Pc Partner will announce results later in August. We already know these results will be very good after a profit alert in June.

We are also looking to get full updates from Greatview Packaging, Sunpower, Straits Trading in the coming 30 days as they report their 1H21 results.

Tiny Beans announced it will be looking to get a dual-listing on Nasdaq as the company’s underlying business is in the US but its listing in Australia. TinyBeans is a small speculative company but could be on the cusp of a large re-rating should a Nasdaq listing be successful. HF&G likes the risk-reward set-up here.

KUKE music was initially dragged down by a sell-off in all Chinese education names but later recovered as investors understood that Kuke’s business model is IN the schools and not OUTSIDE the schools. The government is targeting for-profit tuition centers rather than general education. The key metric to watch the coming week will be if the SmartPiano system is gaining more traction.

ISSP, our Indonesian steel play, continues to do well. The group should benefit from an overall desire for better infrastructure in the entire archipelago. ISSP remains cheap if current results can be sustained going forward.

Last month’s idea mm2 announced it was in discussion to sell its cinema business to Kingsmead. Discussions are at preliminary stage and there is no assurance they will be successful. mm2 is a Singapore re-opening play. Singapore entered another lockdown until the 18th of August so we will have to wait and see if the SG re-opening becomes real in September. If mm2 can sell the cinema business the market should focus its attention on the “content” value of mm2. We estimate this could be 2x the current share price excluding any value for UnUsUal or VividThree.

That’s it for this month. Enjoy August and follow us on Twitter @GreedyHuat for sporadic updates on specific stocks and debunking Covid Hysteria where necessary.