HF&G ISSUE 6 - JULY 2020 - 10 BAGGER

July saw the further appreciation of gold and gold equities as central banks fire up the printing press. In our quest for the next 10-bagger, HF&G names two potential SGX-listed candidates.

First off, if you are on Twitter and like to get more regular updates please look up HF&G @GreedyHuat for sporadic commentary on markets, Covid-19, and stocks on our radar.

HF&G reads several physical newspapers daily (WSJ, Business Times, and FT) and is further informed by various sources such as Bloomberg, a Refinitiv terminal, and websites such as zerohedge.com among many others.

On the 29th of July HF&G burst out laughing reading the opinion pages of the FT which had the following headline:

The article continued:

Gold is not a particularly good investment. It yields no interest and pays no dividend: the only way its owners can earn a return is if other investors value the shiny metal more tomorrow than they did today. For a “haven” asset, which investors can use to preserve capital in times of crisis, it is remarkably speculative: aside from some niche industrial uses, most of the permanent demand comes from jewellery. Its rise in value this week to a near-record high of $2,000 per troy ounce reflects the fact that many other options are even less attractive, rather than any intrinsic merits.

Now, where do we start to pick this apart? Gold is money. Period. Gold has been around for thousands of years and is not controlled by men in suits with a printing press. Historically, HF&G has not been a mindless “gold bug” but to say we are not living by “normal standards” is really what caught us. We are experiencing the weirdest circumstances we have seen in decades and central bankers in Frankfurt, Washington and Tokio have decided to print, print, print their respective currencies like there is no tomorrow. Just look at the below chart (source: Gavekal) how the US Fed’s total assets have grown. Printing has gone parabolic.

HF&G could assume printing our way into prosperity works…but it has never been done before. If this theory “printing-to-prosperity” holds water Venezuela and Zimbabwe would be the world’s richest nations. In 2020 the US M1 Money Supply growth is 33% and the year is not over yet (source: @JeffWeniger). There are already discussions for more printing going on in Washington.

Conclusion: watch what US Fed Chief Jay Powell says himself…

Now after watching this: do you own Gold, and/or other precious metals in your portfolio? As of the 28th of July (source: Crescat Capital), Apple alone is still worth 2.5x the entire market cap of ALL precious metals combined…let that sink in. The weight of gold miners in the S&P 500 is less than 0.5%.

HF&G Performance Driven by Gold

Gold as a commodity is up nearly 20% since we recommended it late March.

Looking back at our stock recommendations so far we note the great performance of all our gold picks: Red 5 is +40%, Bellevue Gold is +167% and Tesoro is +382%.

Before you think: “I missed them, they have already gone up too much”. This is incorrect, particularly for Tesoro. The stock was at 0.074 AUD last month and has doubled in a month…and the best part: it is STILL cheap at only a 48M USD market cap! Just today Tesoro announced it expanded its El Zorro land position significantly. Management is signaling to the market: we think we have found a large deposit, we better own as much of it as we can.

Most gold miner valuation models are based on 1500 USD gold price long term. What if we reset those long term expectations to 1,800 USD or 2,000 USD/oz? All three junior gold plays listed above could be part of an M&A wave at some point. If you are allocating new money to HF&G’s gold picks our order of preference today would be:

1) Tesoro; 2) Red 5 and 3) Bellevue.

One might think: “but everyone already owns gold, it has run its course”. This is unlikely as most large global investors have zero or negligible exposure to gold. The below exercise uses 2018 figures but the conclusion is the same: institutional ownership of gold is not at high levels. Given the world’s (ex-Sweden) idiotic response to COVID (lockdowns infinity) the demands to keep on printing more, and more, and more and more and more…will continue.

Furthermore, our defensive picks (Haw Par and Dairy Farm) have gone absolutely nowhere. Should markets roll-over both should do well. Major Cineplex will eventually open its movie theatres again so we are just patiently waiting. SATS reported some poor FY20 figures (as expected) and remains a long-term bet on travel rebounding at some point in 2021-2022. Don’t expect SATS to perform in the short term, it won’t. Oriental Watch was added late June and will pay a 6.5% dividend yield by the 2nd of September if you buy it today.

Our uranium picks (only available to subscribers) had a strong month in July with most stocks rallying between 25-40%. Become a subscriber and find out which Uranium picks we recommend. The uranium set-up could be even more positive than gold or other precious metals. If you think Tesoro Resources has gone up a lot? The Uranium names might surpass all that once investors start to realize how tight the uranium market has become.

Not a subscriber yet? A subscription costs less than 1 USD/day and one good recommendation can make you back multiple times your annual subscription.

Biden Time or Trump Time?

At the start of August, we are now only four months away from the US elections. US elections always influence global stock market movements so investors better keep track.

Biden is leading Trump by a large margin in all polls…but so was Hillary in 2016. Biden has rarely been seen in public, preferring to hide in his bunker. Biden will announce his Vice-Presidential pick soon and the TV debates are coming closer. These debates could be game-changers as questions are not scripted and “gaffe machine” Biden is a strong competitor to “error-prone” Trump. Maybe the polls will get it right in 2020… or maybe they won’t as predicted by this professor:

Whoever wins one thing seems sure: large deficits and money printing will continue.

Biden’s campaign is surely on the fear-mongering trail. Joe Biden (or at least someone on his team) wrote the following op-ed in The Guardian mid-July.

HF&G is of the view there is no impending climate or agricultural disaster. As a student of history, HF&G is often amazed at how quickly people forget the long list of endless doom prophets who’s predictions never happen. 1980 is a special year for HF&G. Fortunately, we are now in 2020, and Armageddon (as per below predicted by 2000) has still not arrived.

Wanted: 10-Bagger

Before starting huat.co earlier this year HF&G has been publishing views on Smartkarma.com since 2017 and we have unearthed many successful investments particularly in small and mid-cap companies across Asia.

Two of the most successful ones were

China Meidong (1268 HK) and UG Healthcare (UGHC SP)

Both are up 10-fold (1,000%) since we first wrote about them.

Here is Meidong’s first piece when the share price was at 1.55 HKD. Meidong recently closed about 22 HKD.

and UG Healthcare’s first piece when the share price was at 0.20 SGD. The stock recently closed at 2.52 SGD.

NOW….more importantly than looking back: which stocks have 10-bagger potential from today’s levels?

What does it take for a stock to become a 10-bagger? Some common attributes:

Low valuation

Earnings Growth

Multiple Expansion

Right Timing

…and some luck

If one could only predict which exact stocks would become ten baggers in advance.

Just as HF&G has advocated with Gold and Uranium the best is to consider a basket of stocks that could increase 10x.

Here are two elevator pitches for two potential 10-bagger candidates listed on SGX:

#1 Rex International

Rex (REXI SP Equity) is an oil & gas technology company that has evolved into an oil producer.

Rex listed on SGX in July 2013 at 0.50 SGD. Shares were recently trading around 0.18 SGD. Currently, the company has a market valuation of 170 million USD and an Enterprise Value (EV) of just 140 million USD. Rex ADTV is 5 million SGD+ so trading it is not a problem.

Rex is 45% controlled by a group of Scandinavian businessmen who are all in their late 60’s, early 70’s. Rex is their “moonshot” to achieve financial independence for multiple generations.

Rex was originally founded as a virtual drilling technology that helps O&G companies locate wells successfully. Unfortunately, after the IPO the oil price quickly fell from 110 USD to 25 USD in 2016. Exploration activities stopped and Rex’s business went into a tailspin. Rex bottomed at 0.04 SGD in August 2018. The drilling technology has remained but Rex has now added exploration assets in Norway and a producing asset in the Middle-East.

The big Prize: Block 50 in Oman (see picture below). This is the first (shallow) offshore project in Oman that has successfully found oil. Rex owns 86% of the Yumna prospect. The company got its DOC (Declaration of Commerciality) on the 17th of July.

Rex will now start to produce cash flow for the first time in its life as a public company. Assuming oil stays at 40 USD/bbl Rex will generate 40M USD in cash flow by FY21. Rex is therefore currently valued at 3x 2021 cash flow. Rex has no debt.

How does this make Rex a potential 10-bagger?

The prospective area of Block 50 is 17,000 square km (23x size of Singapore). The first well (Yumna) found oil and is producing 10K bbl/day. Rex will drill another well in Yumna later this year and an exploration well further down Block 50 in 1H21. Should these wells find more oil, cash flows could increase materially. The big game-changer is however to prove up the estimated 4 billion barrels of oil which are estimated to be hiding in Block 50. If Rex can demonstrate and bring these reserves from 3P to 1P status the company could potentially be worth 1-2 billion USD at a 60-80 USD oil price. Another wild card is the price of oil. JP Morgan recently predicted oil prices could peak as high as 190 USD/bbl by 2025.

Even if oil prices average 80 USD from 2022-2025, Rex produces 30K/bbl a day in Oman (assumes 3 successful wells) the stock could go up 10-fold. In this scenario, the company could generate 240 million USD in annual cash flow. Putting a 6x multiple on that gets us to a market cap of 1.44 billion USD.

Clearly, there are risks here: the price of oil could collapse to sub 25 USD and make the entire Oman project uneconomical. Rex could stop finding oil in Yumna or anywhere else in Block 50. Management could do something stupid with the cash and spend it on a dumb acquisition. Historically, the company has been prudently managed and never had any debt. The likelihood of Rex being acquired at some point is high.

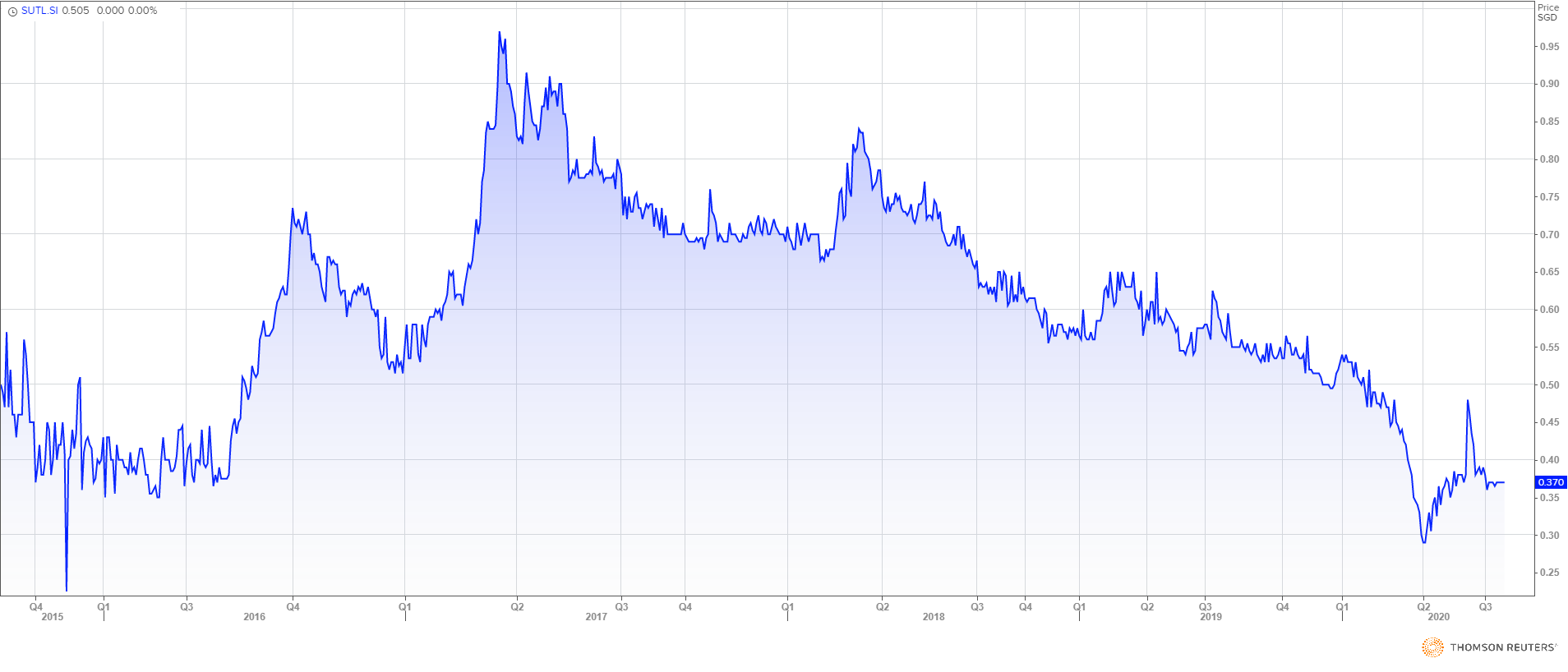

#2 SUTL Enterprise

SUTL has many of the characteristics we saw in UG Healthcare: an orphaned stock, trading at an absurdly low valuation with hardly anyone following the progress of the company. Just like UG Healthcare in 2018, its business expansion has faced delays but the eventual value could be substantial.

SUTL (SUTL SP Equity) is listed on SGX and operates the marina in Sentosa. Sentosa is an island off the Singapore coastline that has a combination of a casino (Genting Resorts World), golf courses, hotels, tourist attractions, residential units, and a marina.

SUTL operates the marina and has the license to operate it until at least 2034. In essence, it is a monopoly that has berthing spots for 270 yachts. Yacht owners pay berthing fees, become part of the One 15 Marina clubhouse, and can use its facilities (swimming pool, kids facilities, bars, restaurants).

SUTL's prime asset is its flagship marina in Sentosa Cove, Singapore. SUTL has only been listed (via a reverse takeover of Achieva Ltd) since 2015 so results prior to that date are not very useful when analyzing the company.

SUTL is led by Arthur Tay (65 years) who was featured in Singapore's Tatler magazine in 2017.

Marina One 15 on Sentosa Cove opened in 2007 and celebrated its 13th anniversary this year. One 15 was awarded Best Marina in Asia from 2016 to 2019.

picture: Sentosa Cove, Singapore

The Singapore asset has 270 wet berths, 14 mega-yachts berths, and 3,800 members. SUTL generates revenues from four sources:

Once yacht owners become members the likelihood they renew their annual membership is high. Unlike cars, which can easily be moved from car-park to car-park, there is simply no comparable alternative in Singapore.

Outside of Singapore, the company is expanding in China, Indonesia, Thailand, Malaysia, and the US. All projects have faced delays in the past but progress continues on most. Covid-19 has clearly put a large dent in advancing projects. Eventually, COVID will be over and SUTL’s assets will come online at some point. By this time they will start to generate recurring revenues and cash flows. The ranks of UHNW Asians continue to grow and wealthy people love to buy expensive assets that depreciate fast (cars, yachts, private jets).

As highlighted above SUTL is currently priced at a NEGATIVE Enterprise Value of 20M SGD. Mr. Market is saying that SUTL is not even worth the cash on its balance sheet and the profitable Sentosa operation has a negative value. HF&G thinks this is highly unrealistic. While you wait the company will pay you an annual 5% dividend yield. ADTV is sub 100K SGD per day, hence use limit orders when buying.

How does this make SUTL a potential 10-bagger?

HF&G believes SUTL has the potential to be worth 320 million SGD in a few year’s time, which would be a 10-fold increase from its paltry 32 million SGD market cap today.

SUTL can achieve this by bringing online a few of the below marina’s which continue to be in various stages of completion. Some are construction sites, others are management contracts.

Once these marina’s complete they will generate berthing and membership fees which will start to add cash flows to its only producing asset as of now (Sentosa). Below one can see that SUTL has been consistently profitable since 2015.

As with any investment, there are risks. Given that you are buying SUTL at a negative enterprise value those risks are low. However, it is possible that the Tay family does not care about maximizing value for minorities and will disappoint on the delivery of its new marina’s. Another risk is that by 2034 its major asset (Sentosa) could not be renewed. Finally, management could do dumb things with the cash on the balance sheet and destroy shareholder value.

That’s it for this month! Enjoy August and see ya’ll soon.