HF&G ISSUE 4 - MAY ISSUE - MINISTRY OF SILLY RULES

HF&G ISSUE 4 - MAY ISSUE - MINISTRY OF SILLY RULES

In this issue, we look at the explosion in silly, non-evidence based Covid19 rules globally and a contrarian travel-related monopoly which is available on the cheap.

First off, if you are on Twitter and like to get more regular updates please look up HF&G @GreedyHuat for sporadic commentary on markets, Covid-19 and stocks on our radar.

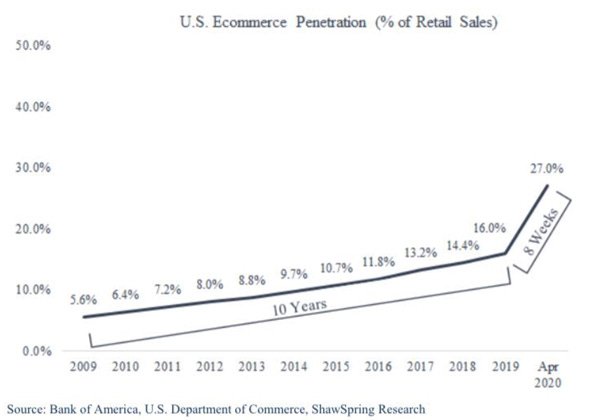

May was a good month for equities globally. Nasdaq is now even positive YTD as flows into FANG stocks continue at record rates. With trillion dollar market caps among many FANGs their rise is supported by fund flows but also e-commerce penetration in the USA has just gone on a J-curve trajectory. If you don’t have a strong online strategy you are toast.

There is a large disconnect between the 1H20 economic data, which is universally horrible (but backward looking), and world equity markets performance (forward looking). As more countries lift their lockdowns economic activity is gradually recovering so news flow will get incrementally better not worse. There is also strong evidence that even if there is a second wave of Covid-19 in the fall many countries (e.g. Denmark, Norway, Belgium, USA) will under no circumstances shutdown again. This raises the economic risks to countries that remain in lockdown or would be tempted to go in lockdown again later this year. Hence, the rebound in economic activity will continue.

We also witness a wall of global money printing being unleashed on equity markets to support asset prices. One can argue if this is wrong or right all day long. Fact: it is happening and the consequences down the road are likely massive inflation at some point. Many economists argue we will witness deflation first. HF&G doesn’t know the answer and neither does anyone else. Prepare for both is the only sound advice.

HF&G Gold Stocks Are Flying

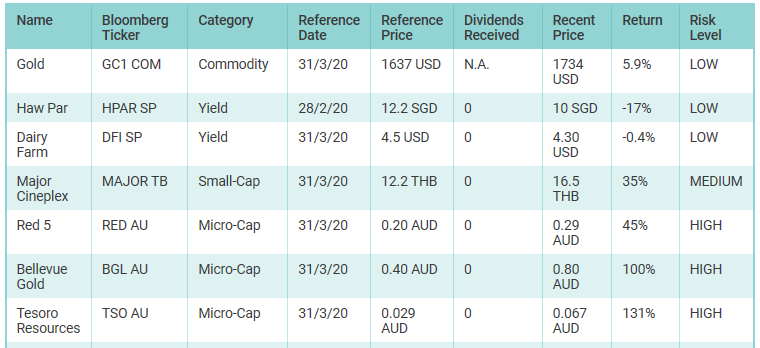

Looking back at our stock recommendations so far we note the unbelievable performance of our three gold picks: Red 5 is up 45%, Bellevue Gold is up 100% and Tesoro Resources is up 131%. The gold price itself is up a respectable 6% in the last two months but as we flagged in our March issue junior gold equities are a turbo charged way to benefit from rising gold prices. In our April issue we also recommended a basket of junior uranium companies which have seen performances of -10% to +20% depending on each company. Subscribers get to see the uranium names selected and additional commentary why these uranium mines could see similar performance as we have already experienced in our gold juniors.

HF&G is not a “get quick rich” scheme. Seeing stocks double in two months time will remain HIGHLY unusual. Our full portfolio review will be published in a separate note only available to subscribers.

Not a subscriber yet? A subscription costs less than 1 USD/day and one good recommendation can make you back multiple times your annual subscription.

Flatten The Fear …Part 2

As we wrote in our April issue HF&G still thinks it is time to Flatten the Fear and realize we overreacted to Covid-19 due to enormous modeling errors by Imperial College and others who scared global policy makers into draconian actions and economically destructive lockdowns. Unbelievable “detached from any economic reality” advice sadly continues:

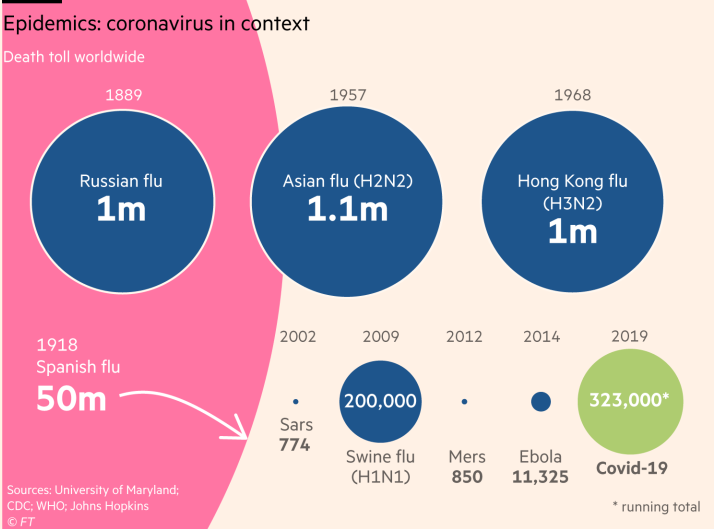

The infographic from the Financial Times (Lex column, FT 23/05/2020) compares the Covid-19 deaths YTD versus the 1968 pandemic (no lockdowns) and 1957 pandemic (no lockdowns). Sure, Covid-19 deaths will go up but will they still triple from here? Is the counting too high or too low? We will find out over time.

Another aspect of this pandemic that is unprecedented is that the UN estimates 500 million kids (yes that is 500,000,000 children vs 323,000 deaths) are out of school despite the fact that they are least at risk. From official WHO and CDC data we now learn that the risk of death from Covid-19 for children below 25 years old is 0.00008%, or roughly 1 in 1,250,000.

Ministry of Silly Rules

In the 1970’s the hit TV show was Monthy Python. One of its more famous episodes is the Ministry of Silly Walks.

Fast forward to 2020 and the global political elite seems to have gone in complete overdrive to create a plethora of silly rules which are not evidence based but instilled by fear and the desire to “do something” against Covid-19.

A non-exhaustive list we have collected from across the world:

No better way to start this list than Nassau’s county rules for playing tennis. Remember, this is not stand-up comedy but real-life.

in Thailand it seems to have been decided that massages are allowed from the waist down. Massaging of the neck or upper body are “too risky”.

in Belgium it was finally agreed that grandparents could see their grandchildren again but hugging was not allowed for more than 15 minutes. Get out your stopwatch grandparents!

in Denmark the government reduced the mandated social distancing rule from 2 meter to 1 meter in April. Why was it 2 meter to begin with? Will 1 meter be enough? Why not 1.7 meter? Why not 1.3 meter? Evidence based, anyone?

in Japan gyms are allowed to re-open but one cannot run faster than 10km/h on a treadmill, group classes are limited to five people and no high-fives are allowed. Intensive activity in pools is not allowed. Masks are required in karaoke rooms “except when you are singing or eating”. Is this a South Park episode?

school children globally are, depending on their location, slowly returning to schools and have proven to be at little risk from catching or spreading Covid-19 yet school bodies are going overboard to implement mask wearing and social distancing among toddlers as young as 2 years old. The US CDC also advocates to close playgrounds and communal spaces. Has any study been done to show if this will accomplish anything except make the job of teaching small kids virtually impossible? Isn’t part of being a kid growing up and being exposed to viruses so your immune system can built? Should kids be protected in bubble wrap so they can surely not get any disease or virus at any point?

across the world many public transport commuters have been asked not to talk while in public transport despite already wearing masks. We are waiting for the announcement that regulates, and enforces, breathing is only allowed via the left nostril on Tuesday and the right nostril on Wednesday.

HF&G asks itself: is there a global WhatsApp group where political leaders meet to concoct these zero-evidence based rules? Does anyone even care about their effectiveness or have we now gone the way of Emperor Joseph II in the 1700’s? Emperor Joseph II ruled over the Austrian Habsburg empire for a few decades but was best known for micro-managing every little detail of his constituents up until the most minute detail. Let’s just say he wasn’t very well liked.

Wouldn’t it be more effective to have three rules globally that are clear such as 1) wash hands, 2) wear a mask when ill or in a crowded indoor place, 3) stay home when your sick. Humans will listen and be understanding for easy and simple rules but will flaunt rules that lack common sense and are hard to implement let alone control.

Meanwhile to finish on the topic of Covid-19. Our overreaction to this pandemic is becoming clearer by the day. Study after study now show that the vast majority of all cases is among elderly (75+ years old) with pre-existing conditions. If you get Covid the chances you survive Covid for the world population are 99.5%+! As stated last month: let’s also stop the idiocy of saying “we need a vaccine” before going back to normal. Newsflash: there might never be a vaccine. “More than 30 years after scientists isolated HIV, the virus that causes Aids, we have no vaccine. The dengue fever virus was identified in 1943, the first vaccine was approved last year(..) The fastest vaccine ever developed was for mumps. It took 4 years.”

Let’s flatten the fear and start enjoying life again instead of hiding inside. Some vitamin D might actually be an important contributor to fighting Covid according to studies.

This bring us to to the travel and hospitality sector…

“The most money in investing comes from when a situation goes from hopelessly fu**ed to sort of shitty.

Harris Kupperman, Praetorian Capital

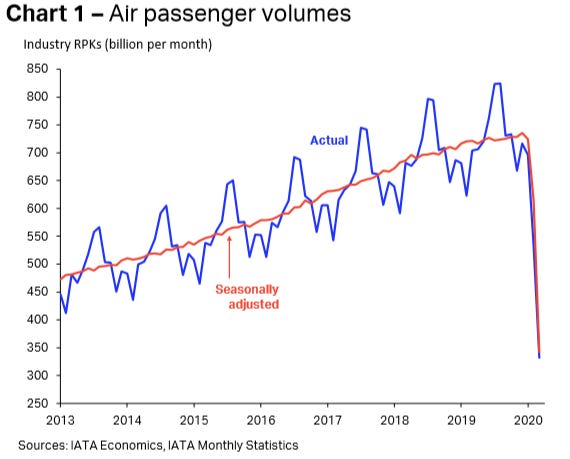

Can we think of an industry that is more screwed than hospitality and travel? In April Singapore airport operator Changi Airport reported that passenger traffic was down 99.5% YoY. It can’t get much worse than -99.5%.

IATA has put of the following graph which needs little explanation: things are bad if you have anything to do with travel and hospitality.

HF&G believes it is wrong to believe the apocalyptic view of future travel demand. HF&G believes travel will come back. It is just a question of when… and that “when” is determined more by government policies (example: 14-day quarantine rules, airport shutdowns or a silly rules bonanza once you get to airport or aircraft) than an underlying reluctance to travel.

The best example to illustrate our point is demand for cruise liners. Given how hard the cruise line industry has been hit one would expect this category to be dead, right? Nothing is further from the truth with customer demand back to 80% at Royal Carribean for 2020 and 2021 bookings already.

Sure, corporate customers will be the slower to fly again but do not be fooled by the assertion that doing Zoom calls will change everything. Zoom calls are NOT a new invention. We have had corporate video call systems for decades (Polycom and Cisco have dominated this space for the past twenty years) yet this has not stopped people from flying across the world to see each other for leisure or business. Anyone who has tried to attend an AGM or group meeting via Zoom should understand these meetings are suboptimal. Corporate travel demand won’t come back instantly but leisure demand (IF ALLOWED) will be back. We are already seeing this trend in the USA with hotel bookings recovering from record low levels.

Finally, people forget quickly. We saw this after every terrorist or other travel disruption event in the past. Don’t believe the hysteria: Covid will be no different.

So what travel related stocks should we invest in? Short answer:

Own Travel Monopolies

Airlines are generally terrible businesses and Warren Buffett earlier in May sold out of all his US airline investments. If one wants to bet on airlines recovering in Asia AirAsia could be a bombed out (-55% YTD) bet that is likely to survive.

However, HF&G thinks there is a group of businesses that are much better to look at: airport operators and airport services. In Thailand look at Airports of Thailand (AOT TB Equity) or in Malaysia consider Malaysia Airports Holdings (MAHB MK Equity). AOT is down 18% YTD and MAHB is down 36% YTD.

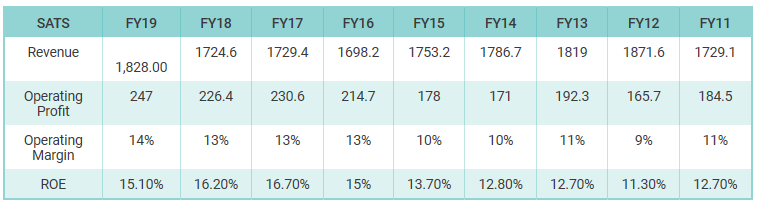

Our preference in this travel sell-off goes to Singapore listed SATS (SATS SP Equity), which has a market cap of 3.1 billion SGD or 2.2 billion USD. SATS had its IPO in 2000, is part of the STI Index and ADTV is over 15M USD/day. SATS has declined by a similar percentage compared to AirAsia but is a much better business. SATS financial year ends on 31 March so its full year figures should be announced any day now.

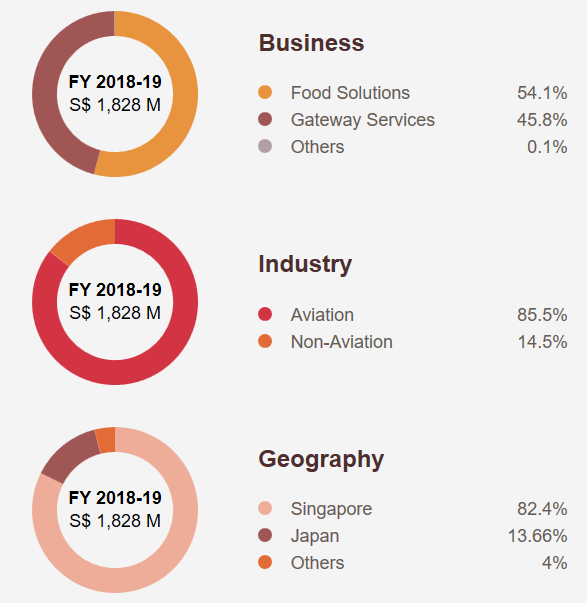

SATS is the dominant operator at Singapore’s main airport (80% market share). Changi is among the top-20 busiest airports as it welcomed 68.3 million passengers in 2019. SATS business consists mainly of food solutions for Singapore based aviation customers (see details below). The biggest customer is Singapore Airlines which has just completed a 15 billion SGD rights issue underwritten by Temasek. Singapore Airlines will survive and we think it is unlikely it will renegotiate its contracts with SATS. Temasek is an owner in both and having just rescued one (SIA) we can’t see how it makes sense to ruin the economics in the other (SATS).

We will be adding SATS to our YIELD portfolio as it has been paying dividends consistently since 2000. The yellow dots on the graph below highlight every time SATS has paid a dividend.

Or looked at in another way between 2000 and 2019 the company paid cumulative dividends of 3.088 SGD/share. Historically the company has paid out over 70% of earnings to shareholders.

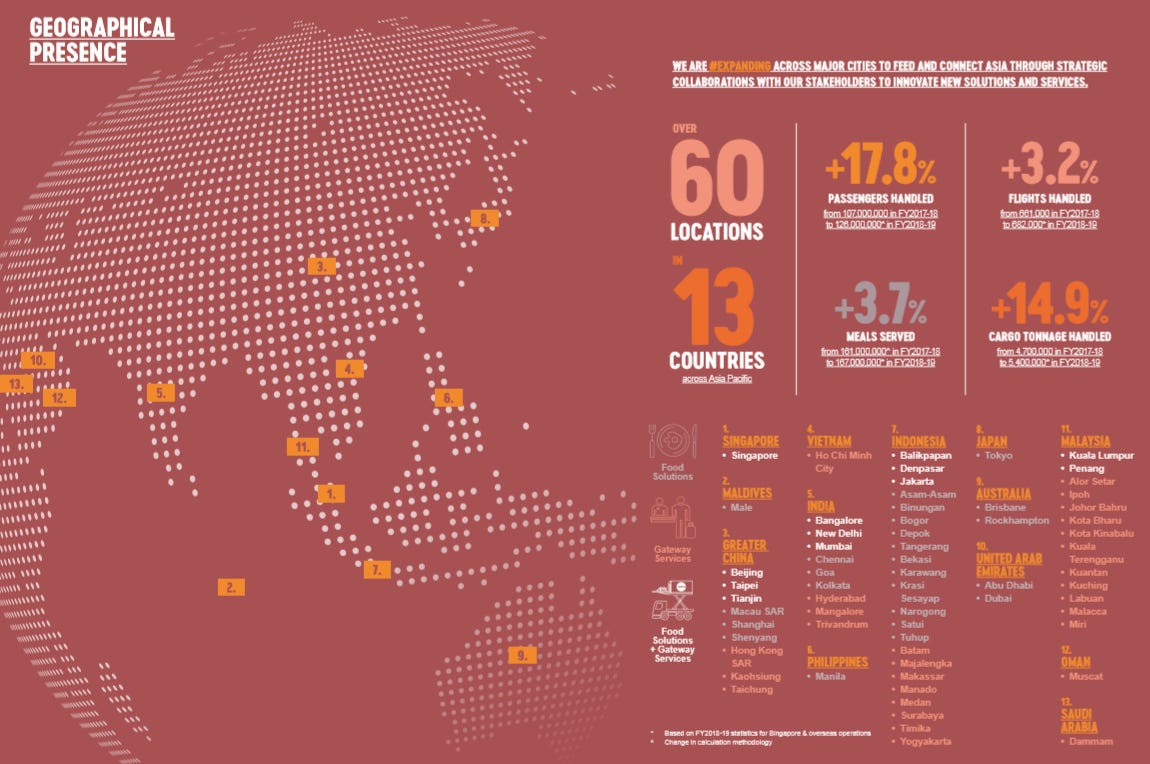

As we demonstrated back in March with Major Cineplex and Dairy Farm we are sure that little dividends will be paid by SATS in 2020. However, if we assume that 0.19c dividend can be restored as of FY22 and those dividends would never rise we would get back our investment in SATS in 15 years (0.19 SGD * 15 years = 2.85 SGD). Again, this is not our projection but a back of the envelope way to demonstrate why investing in SATS is now an attractive idea if one believes in APAC air travel between 2021 and 2035. As shown on page 19 of its FY19 annual report SATS is truly a regional player.

SATS is Attractively Valued

Now the most common push back will be:

“SATS is historically a good business but the next three quarter results are going to be terrible, I will only invest once results improve”.

HF&G believes that all investors in SATS already know that short term results will be terrible. It is priced in. One cannot buy great monopolistic businesses at cheap valuations when everything is going great. Once we get to January 2021 investors will start to look at forecasts for FY22 and FY23. HF&G believes that by that time investors will start to price in a recovery scenario for global travel and SATS will be a liquid, high-quality stock seeing investor inflows. It is really that simple. In investing many things are over complicated.

The risk to SATS doing well as an investment is the continued closure of Changi airport and its other investments in Malaysia, China, India and Japan. A much slower than expected travel rebound could also harm prospects.

The upside case is if SATS does any of the following things:

starts catering for elderly people as Covid-19 will accelerate safety measures around retirement homes and this will include safe meal delivery. SATS is well placed given its stringent airplane requirments

wins contract for AirIndia catering and ground handling services. AirIndia is finally going to have a real restructuring and if Tata/Singapore Airlines are involved via Vistara this business could end up with SATS down the line. Entering the Indian market in a big way would unleash a bonanza of profits a few years down the line

uses its strong balance sheet to make further accretive acquisitions

Over the past decade SATS has traded at an average P/E multiple of 18.8x. We expect FY20 and FY21 figures to be impacted severely with profits down anywhere between -40% to -60%. If we look at FY19 profits as a base case, which could be repeated as early as FY22, the stock is now for sale at 11.8x P/E and a 7% dividend yield. The last time SATS traded at similar multiples was in May 2011. SATS balance sheet is super healthy with virtually no debt. Debt might increase somewhat in 2020 and 2021 but we don’t expect that to cause any major issues.

That’s it for this month! Stay safe and healthy and our next update will come late June.

Final Note: as we are continuously looking to improve HF&G please let us know your thoughts or suggestions in the comment section OR email us at contact@huat.co