HF & G - ISSUE 12 - JANUARY 2021 - GMO VS BTC

GMO rings the alarm of a market top; Bitcoin is exploding higher as the "3am Trade" goes global and this month we are giving you a "tiny" stock idea with big upside.

Happy 2021! The year has certainly started well with markets roaring higher globally. Senior Citizen Joe is now in the White House and is ready to throw the proverbial gasoline on the Fed printing press.

HF&G would like to caution readers again about investing your hard-earned dollars in high-flying US tech companies. We are unsure if we are in March 1999 or March 2000 but valuations, speculation, IPO’s, SPACs, massive retail gambling all point to heavily stretched levels on US exchanges. HF&G focuses on Asian small/mid caps and Asian yield but the temptation to dabble in roaring US markets is high.

A few warning signs in three charts:

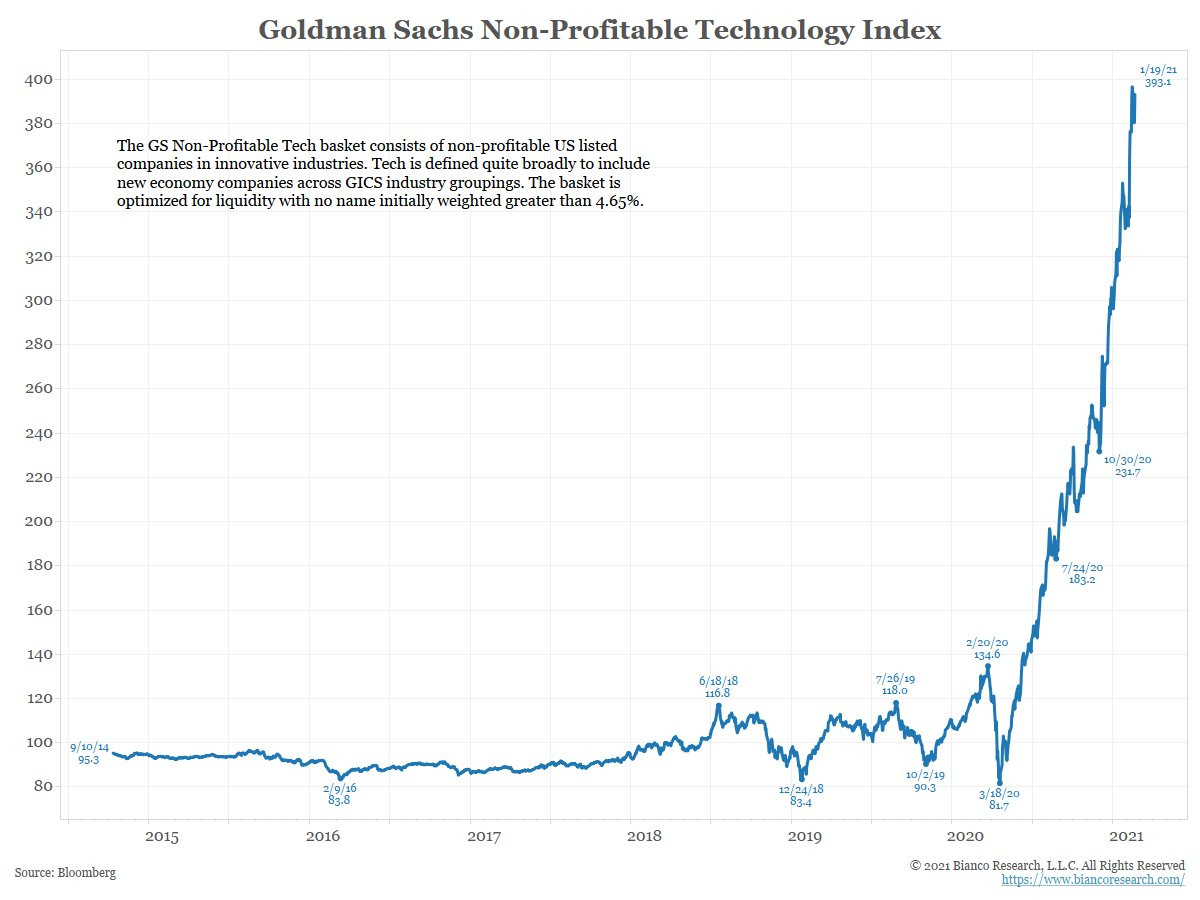

Goldman’s Non-Profitable Technology index is at all-time highs.

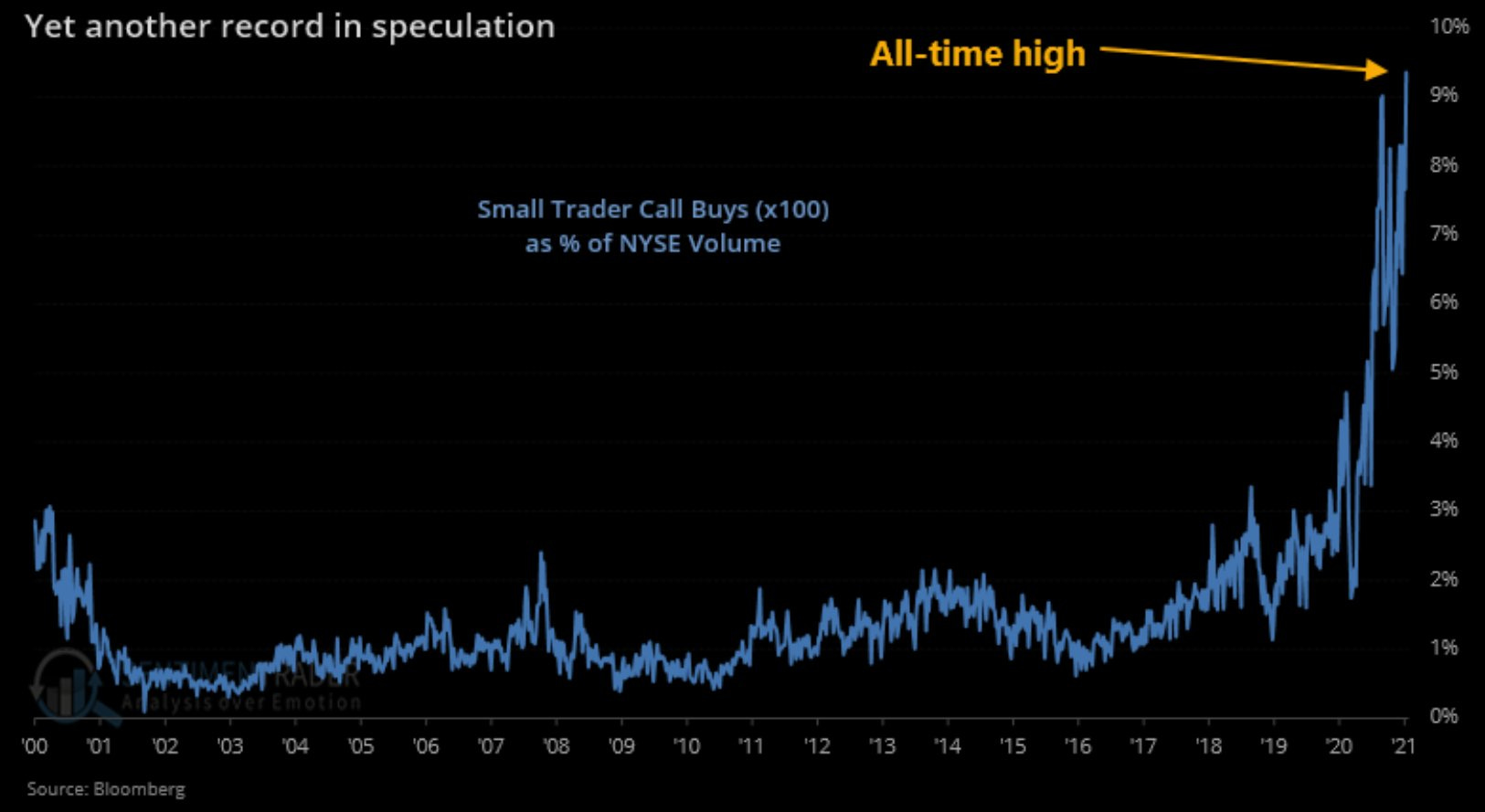

and small investors are buying call options at record levels… GameStop anyone?

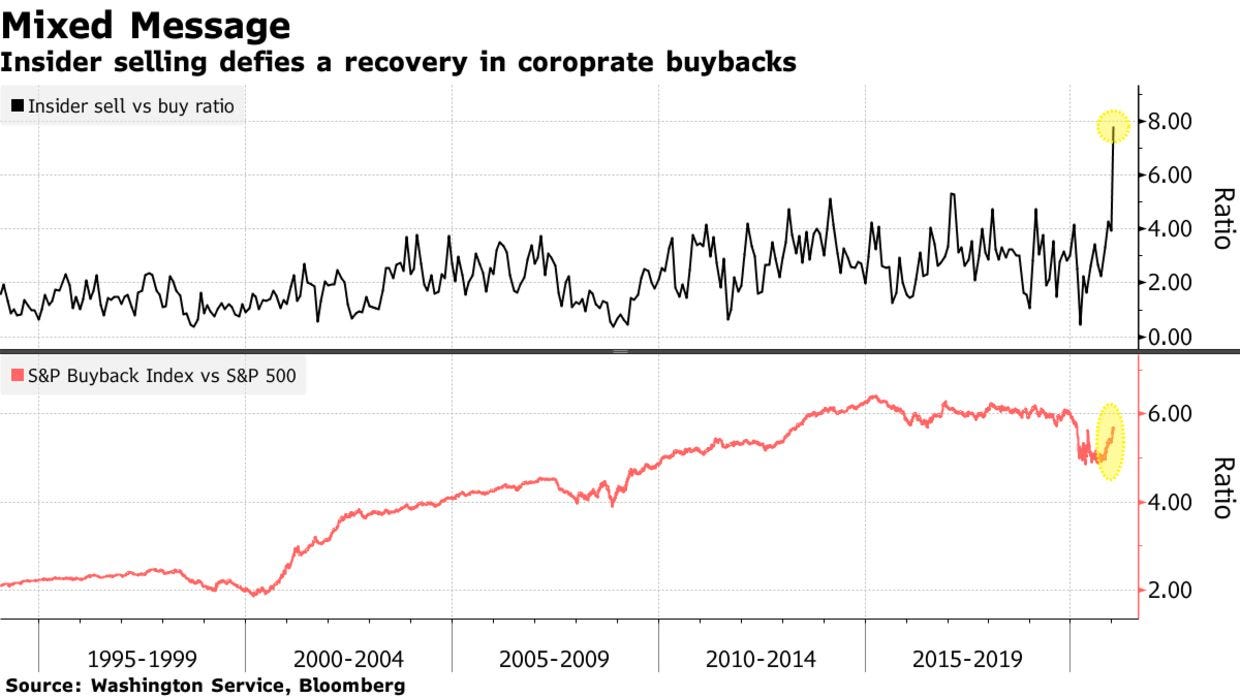

while insiders (company executives) are selling their stock.

GMO vs BTC

Bitcoin is shooting higher as it’s the only financially traded asset that’s available 24/7. With lockdowns all over the Western world and everyone drowning their sorrows in alcohol or other substances, one can just imagine the financial decisions that are being made under the influence of narcotics or alcohol. Peak intoxication comes around 3am so what asset is for sale? Crypto Tulips! Any and all of them. All other markets are closed. HF&G will call it the “3am Trade”. The sky is the limit. Debates on Bitcoin continue to rage with a new (or some say old) hypothesis about Tether and its impact on Bitcoin’s rise. HF&G continues to advocate some exposure as the Tulips are outside the traditional financial system and with the “Build Back Better” crowd now in charge you want to hedge your bets.

On the complete opposite spectrum of Crypto Tulips, we have GMO. A well-respected asset management firm where the founder Jeremy Grantham has called many market bubbles over the decades. In his latest missive (published 05/01/2021) he thinks the 2021 bubble will be comparable to 1929, 2000, and 2008. This means an epic burst in the technology space. Please remember Nasdaq dropped 82% in 2000. HF&G agrees with GMO this can happen again! Who will benefit? Commodities and Emerging Markets value stocks. It is probably confirmation bias but this is exactly how HF&G has been positioned since the launch of our letter about a year ago.

Now, everyone investing should know full well that if the Nasdaq starts to roll-over aggressively (think a 10-15% drop in a week) this will shake markets globally. All the money going into the index trades will come out. Fortunes will be made (and lost) when the tech space implodes. HF&G is not arguing all these companies are frauds and will go to zero but many of them could see their share prices cut by 50% and they still wouldn’t be cheap by any measure. If you own companies that trade at 25x revenues (Tesla), 43x revenues (Nio), 22x revenues (Nvidia), 52x revenues (Shopify) you are warned.

We have seen this movie before in 2000. Sun Microsystems, the darling of two decades ago, traded at 10x revenues. Two years later the stock was trading 90% lower and the CEO, Scott McNeely, analyzed it brilliantly:

“At 10x revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Mutated Nonsense

While stock markets go crazy in the “real world” most countries continue to struggle to control the flu that’s been with us for over a year now.

Recall this? It is exactly one year ago.

So the WHO advocating it was not human-to-human transmissible 12 short months ago has now morphed into a D-A-I-L-Y panic broadcast.

Yes, you have read it. Every day. Every hour. The Covid-19 virus, (SIDE NOTE! which does not kill 99.99% of the global population but has somehow convinced global governments to go apeshit en masse), has mutated. Run for the hills! Jump in the ocean! Whatever you do; please lose your mind about the British variant, the South African variant, the Brazilian variant …every country wants to have its own. It is like the FIFA World Cup.

Speak to any intelligent doctor and they will tell you every virus has on average 400 mutations. It is normal. It is standard. But for Covid-19 we throw everything we have learned for decades out of the window and just live in panic mode. Once again let us repeat: for a person below 65 years old the chances of dying from covid are about the same as dying in a car accident (source: WHO peer-reviewed study by Stanford Professor Ionnadis).

A large study by Penn University recently concluded coronaviruses always become more contagious but this does not make them more harmful or deadly. On the contrary, viruses that spread faster do become less lethal over time. The global press corp on the one hand chastises Donald Trump for spreading fake news and telling falsehoods yet on the other hand copy/pastes any headline that spreads unnecessary fear about Covid without the slightest investigatory and independent mindset. The latest paper about the British variant called B.117 was co-authored by discredited scientist Neill Ferguson of Imperial College.

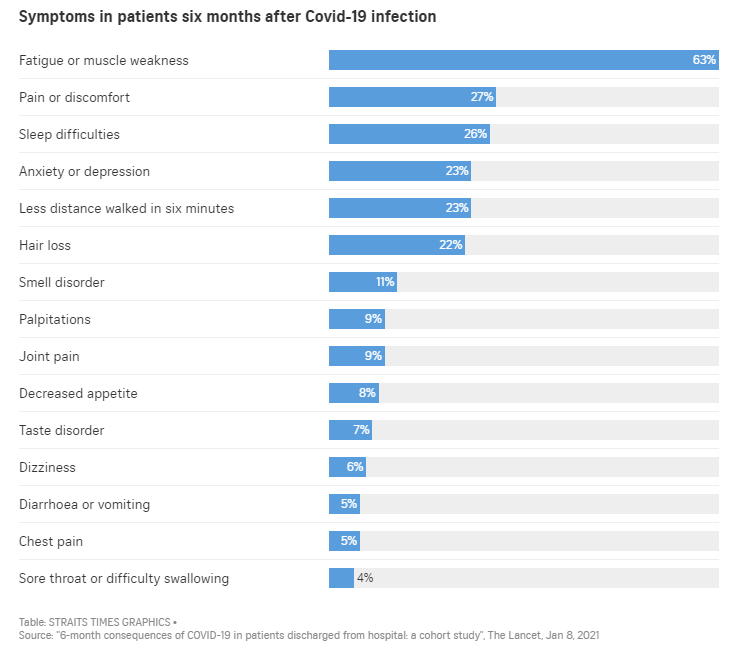

The second absurdity seems “Long Covid” (see below list). As with any disease or ailment, it is very possible there are longer-term hindrances or side effects. So basically if you are tired, have sleep difficulties, hair loss, can’t walk fast: IT IS ALL COVID! How can this even be published in the Lancet? Do we have an honest data set of what the ailments were of these patients before? The general public is told to “trust the science” but how can that be achieved when these recording of symptoms could be due to anything.

If you are very overweight because of bad eating habits you were probably already 1)fatigued, 2) in “pain” to tie your shoes, 3) did not sleep well because of excess kilo’s to carry around and could not walk very fast. Did Covid really make these issues worse? How was this measured? How can they have known what the true state of the people was before? Has it occurred to anyone that sleep difficulties might be due to excess usage of electronic devices or that anxiety and depression might be caused because of all the lockdowns?

Finally, to all the “lockdown-lovers” out there new research suggests it is all pointless.

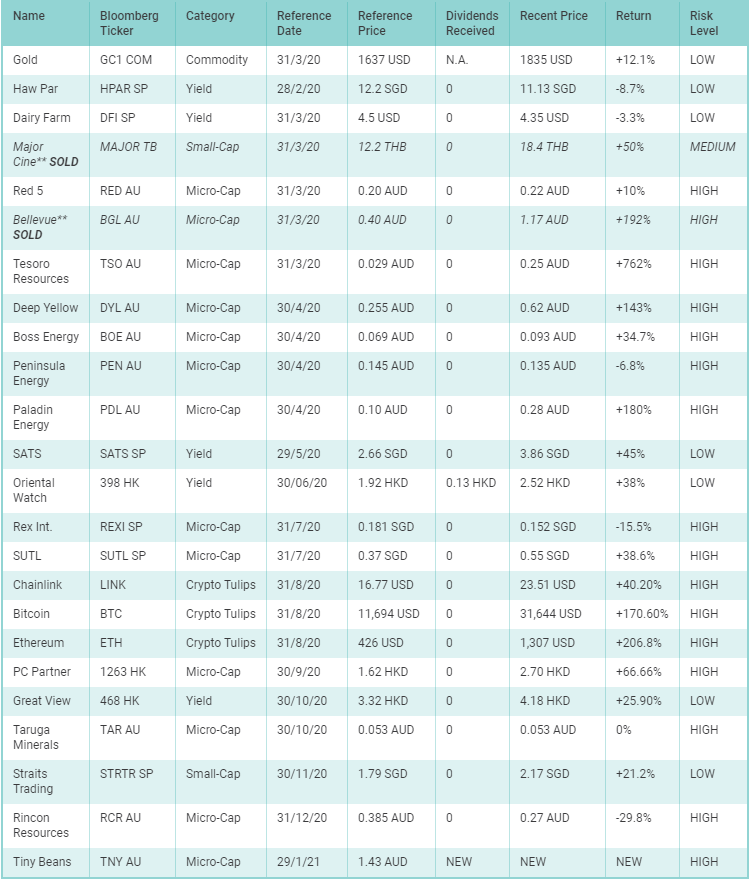

PORTFOLIO REVIEW

January was mostly a good month for HF&G picks. The best performer was Chainlink which effectively doubled from 12 USD late 2020 to 24 USD late January. A victory lap for all the Chainlink marines and applause for their perennial cheerleader BenV. The junior uranium names followed suit and ripped higher.

After taking our profit in Bellevue Gold last year, we are now also advocating to get out of Major Cineplex, Thailand’s dominant movie theater operator. Major Cineplex has historically been a fantastic business but the continued rise of streaming (Disney+, Netflix, etc) is unstoppable and makes us worry about Major’s long-term trajectory. The transformation to streaming might be slower in Thailand vs Europe or the US but we prefer to watch this unfold from the sidelines. The stock is very liquid and has gained 50% since we recommended it in March 2020. Overall a great return in less than 12 months.

As our subscriber base grows we will be gradually giving more content that is only available to paying members. Don’t want to miss a thing? Take a subscription for less than 1 USD/day.

Tiny Stock Idea

Any young parent knows when they look in the image folder of their smartphone: it is full of pictures and videos from their children. Every minute of a baby’s life is now documented in still or moving images. While travel is complicated and family members and friends are not able to get together these images are being shared in WhatsApp groups. With Zuckerberg intent on exploiting every image your share on WhatsApp for his personal gain, the importance of privacy has led to an explosion of downloads for Signal and Telegram.

But what if there was an app that focused solely on young children and allowed you to share experiences, pictures, and videos among friends and family in a safe and organized way: enter TinyBeans (Bloomberg ticker: TNY AU Equity).

We also want to give credit and a hat-tip to A.B. in Cape Town for initially bringing the company to our attention.

The company was founded in 2013 and until today is led by Eddie Geller. The company has amassed 5 million users (4.8 million monthly active users) +253% higher than last year. Tiny Beans runs a free product and a paid version. 92% of paid users have renewed their purchase once they started using it.

Tinybeans’ strategy is two-fold: grow subscribers and increase ad spending. In order to drive this, it has hired senior executives from Amazon and Disney+ over the last few months. It is these hires that attracted our attention since we started following the company about six months ago.

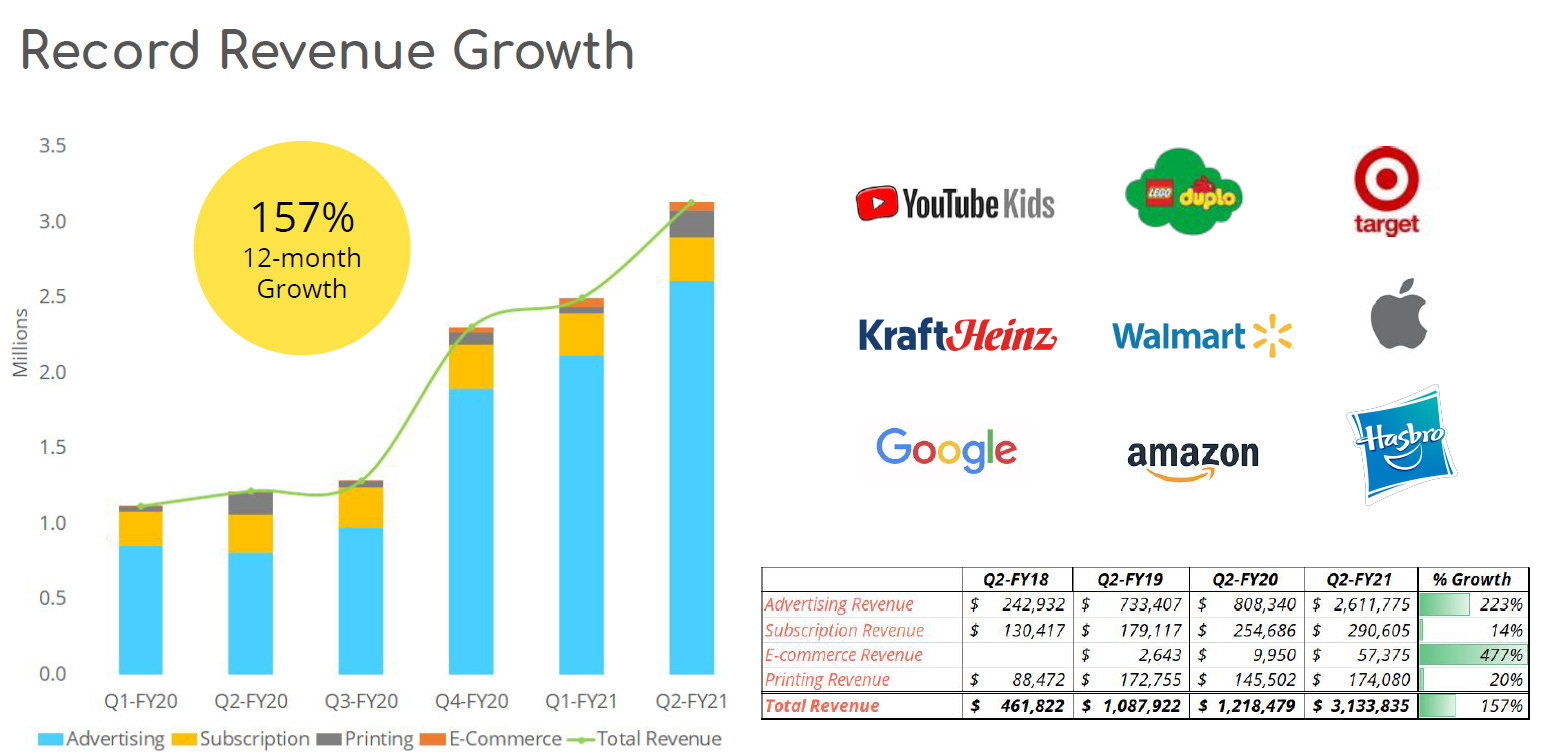

Tinybeans announced its 2Q21 results (October-December quarter) last week and they showed continued growth in all segments. The caliber of advertisers has also grown significantly.

What makes Tinybeans attractive to an investor is that we are buying a platform company that is experiencing a flywheel effect. More users = more advertisers = more word of mouth marketing = more engagement = better product = better financial results.

Tinybeans last year bought RedTricycle and is now going to integrate it into their platform. Later in 2021, it will add subscription services and it will aim to monetize its user base. If a small percentage of its users is willing to spend 1 or 2 USD/ month to received curated content the opportunity could be large. Obviously, it is not guaranteed this strategy will work but we are currently not paying much to see where this goes.

Why is Tinybeans cheap? It is lost on the ASX while its business is virtually all US. We are sure if this story gets re-listed on Nasdaq the company would trade at 2-4x its current valuation (meaning a market cap between 100-200 million USD). Platform companies trade at a multiple of Monthly Average Users (MAU) and on this metric, Tinybeans is cheap (50M USD mkt cap/4.8 million MAU).

Tinybeans was recently trading at 1.43 AUD/share which equates to a market cap of 65 million AUD or 50 million USD. Tinybeans has no debt and five million AUD in the bank. HF&G thinks this is too cheap if the company continues to deliver on its growth trajectory.

The risk here is failed execution by the management team, being unable to re-list on a US exchange, and staying hidden (and tiny!) forever. We will take our chances and bet that Eddie and his management team (who are significant shareholders) will find a way to unlock value.

That’s it for this month. See you all after Chinese New Year for another update late February. As always you can find us on Twitter @GreedyHuat.