HF&G - FEBRUARY 2022 - A SMALL NUCLEAR WAR TO COOL THE PLANET?

HF&G - FEBRUARY 2022 - A SMALL NUCLEAR WAR TO COOL THE PLANET?

With Russia preparing its nuclear arsenal a surprising call to use them might come from the "climate" lobby; a portfolio review highlights our top picks and pans.

The shortest month of the year proved the most volatile. The invasion of Ukraine by Russia, right after the Chinese Winter Olympics concluded, caught investors by surprise. While tensions had been brewing for months many believed Russian President Putin was just flexing his muscle but would hold back on an actual invasion. Putin proved many pundits wrong with his brazen invasion of Ukraine. As of this writing, Russia is not in complete control as Ukrainian forces are mounting increased opposition. Western countries have imposed economic sanctions which have crashed Russian stocks and cut its currency by nearly 50%. The exclusion of Russia from the SWIFT banking system is painful for Russian business. HF&G has never advocated buying any Russian stocks and is not tempted by the current weakness. Investing in Russia is even more complex than investing in China.

The entire Russian uncertainty has propelled oil & gas prices higher and supported the gold price. Russia is a significant commodity exporter and the unpredictable behavior of Putin has caused major headaches in Europe. Why?

Let’s look at the % share of natural gas supply from Russia to some of its European neighbors:

Finland 94%, Latvia 93%, Bulgaria 77%, 49% Germany, 46% Italy, 40% Poland, 24% France, 11% Netherlands, 10% Romania.

European gas prices are now 30 USD/mmbtu vs 4.5 USD/mmbtu in the USA.

Germany is the clear standout here as it is closing its nuclear power plants, invested 125 GW in solar and wind power yet in many days uses only 5-10 GW of this capacity. The shortfall is made up by Russian gas and German&Polish brown coal (no joke!). Germany has a new government where the Green party plays an integral role and they want to double down on the “green” climate religion. HF&G calls it a religion as there is no room for rational debate around the topics of energy security and changes in climate.

Failed EU green policies, which have cost hundreds of billions of euro’s in subsidies over the past two decades, but have not yielded any savings to energy consumers are now coming back to bite EU policymakers. The simply idiotic policies by many countries (excluding France) to shut down baseload nuclear power in favor of unstable renewables is a klusterf*ck of epic proportions. These policies also can’t be easily reversed as several industries are now dependent on these subsidy revenue streams. An entire system of “carbon credits” has been created so “air” in one country can be sold to another country in order to feel good (Look at me I am so Green!) and claim to be “Net Zero” or some other “Green” economy gibberish. The bottom line for investors: the green transition will happen but at a much slower pace than people expect. This means traditional commodities (oil, uranium, gas, coal, copper, zinc, etc) are likely to enjoy multiple years of excellent returns at the exact same time that large funds have been forced to sell these commodity shares. This explains why most of these traditional commodity players trade at single-digit P/E and cash flow multiples. A multi-year re-rating could be on the horizon and retail investors can profit handsomely. On the flipside, structurally higher energy prices are going to hurt all consumers and risk keeping inflation elevated.

Even while tanks are rolling in Kyiv the chief European green economy apostle, Frans Timmermans, continues to insist the old continent’s biggest issue is global warming. The delusional leader might like a study from National Geographic which questioned what effect a small nuclear war would have on global warming. Heaven forbid Extinction Rebellion, Frans Timmermans or John Kerry get a hold of the nuclear codes, they might try their luck trying to test the hypothesis.

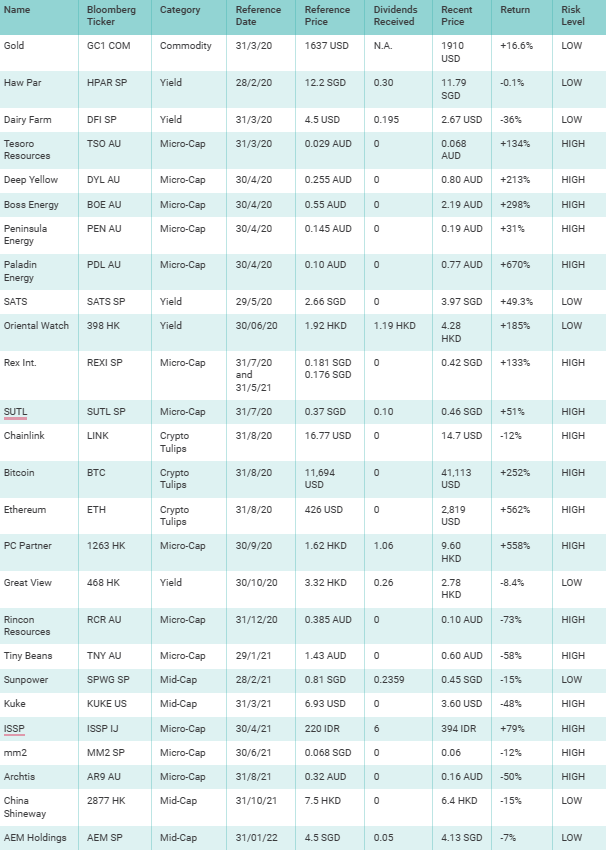

PORTFOLIO REVIEW

Our uranium basket continues to perform super strong with our stocks up between +31 to +670%. We recommended SGX listed oil play Rex International both in July 2020 and in May 2021. The stock has doubled from those levels and recently closed at 0.42 SGD. It needs little explanation that at the current 100 USD oil price Rex will be printing cash faster than a casino. Despite the recent slump, our basket of crypto’s is up overall, except Chainlink which is down marginally. If you are looking to put new dollars to work HF&G would advocate buying a position in PC Partner after the recent weakness. Results in late March should be a catalyst on top of a very large dividend announcement. This month we will be saying goodbye to Straits Trading after the stock was up 82% over 15 months. Why are we selling? Management raised a lot of capital via a placement to buy two properties in Melbourne. The transaction made no sense to us and when Asian management teams do erratic things we run for the hills. Another strong candidate to be axed is China Shineway. While the board announced in July 2021 it was instituting a very sensible dividend policy it canceled the same policy in December 2021. The downside is well protected by the 6 HKD cash on the balance sheet (vs 6.7 HKD share price) but we have seen too many of those HK stories where the cash never ends up in the pockets of minority shareholders. We will keep China Shineway until its full-year results are published in late March and make a decision to hold or axe it.

In micro-cap land, our positions in Tesoro and Rincon resources have deflated significantly despite a rising gold price. Since they are junior exploration companies that do not produce any gold this is likely caused by the disappointment in the management team. Both management teams have overpromised and underdelivered. Tesoro should be updating its resource estimate in the coming 45 days which could prove a catalyst. Our stock pick from January 2022, AEM Holdings, went south even though it published solid FY21 figures and a bullish outlook. HF&G thinks the market is wrong and the stock doubles from here once investors understand the uniqueness of the company as a prime beneficiary of Intel’s capex expansion. At some point, AEM also becomes a prime M&A candidate. Given the high level of volatility and uncertainty, we will not be adding any names to our selection this month. Preserving cash is also a strategy.

That’s it for this month! Enjoy March and let’s hope Vladimir, Frans and John keep the nuke’s in check.